For many small businesses, late payments aren’t an inconvenience—they are a liquidity test. The gap between issuing an invoice and receiving funds can disrupt payroll, delay growth decisions, and introduce ongoing financial strain.

According to Bluevine’s February 2026 survey of 1,052 U.S. small business owners, nearly 3 in 10 delayed paying themselves because customers paid late. The findings show that delayed payments often leave business owners juggling cash flow needs.

For firms operating on tight margins, even short delays can ripple outward into payroll decisions, personal compensation, and long-term planning. In many cases, owners absorb the shock themselves.

Key takeaways

59% of SMBs experience at least occasional late payments, which means delays are widespread, not isolated.

28% have $5,000+ tied up in unpaid invoices—a substantial share of revenue for many businesses earning under $100,000 per year.

17% of SMBs have missed payroll or nearly missed it due to late payments—linking receivable delays directly to employee paychecks.

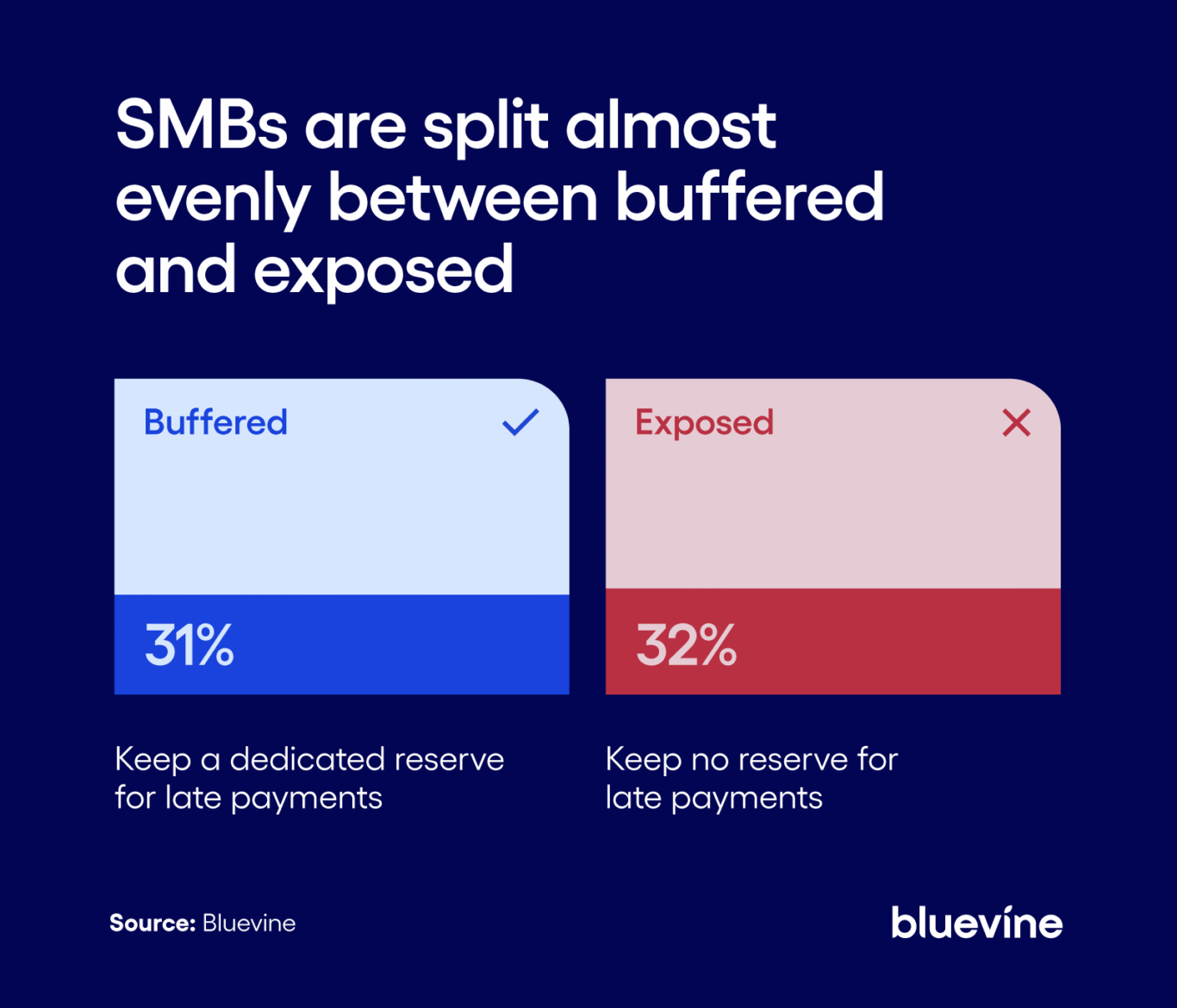

Only 31% keep a dedicated reserve for late payments, while 32% keep none, splitting SMBs into buffered and exposed camps.

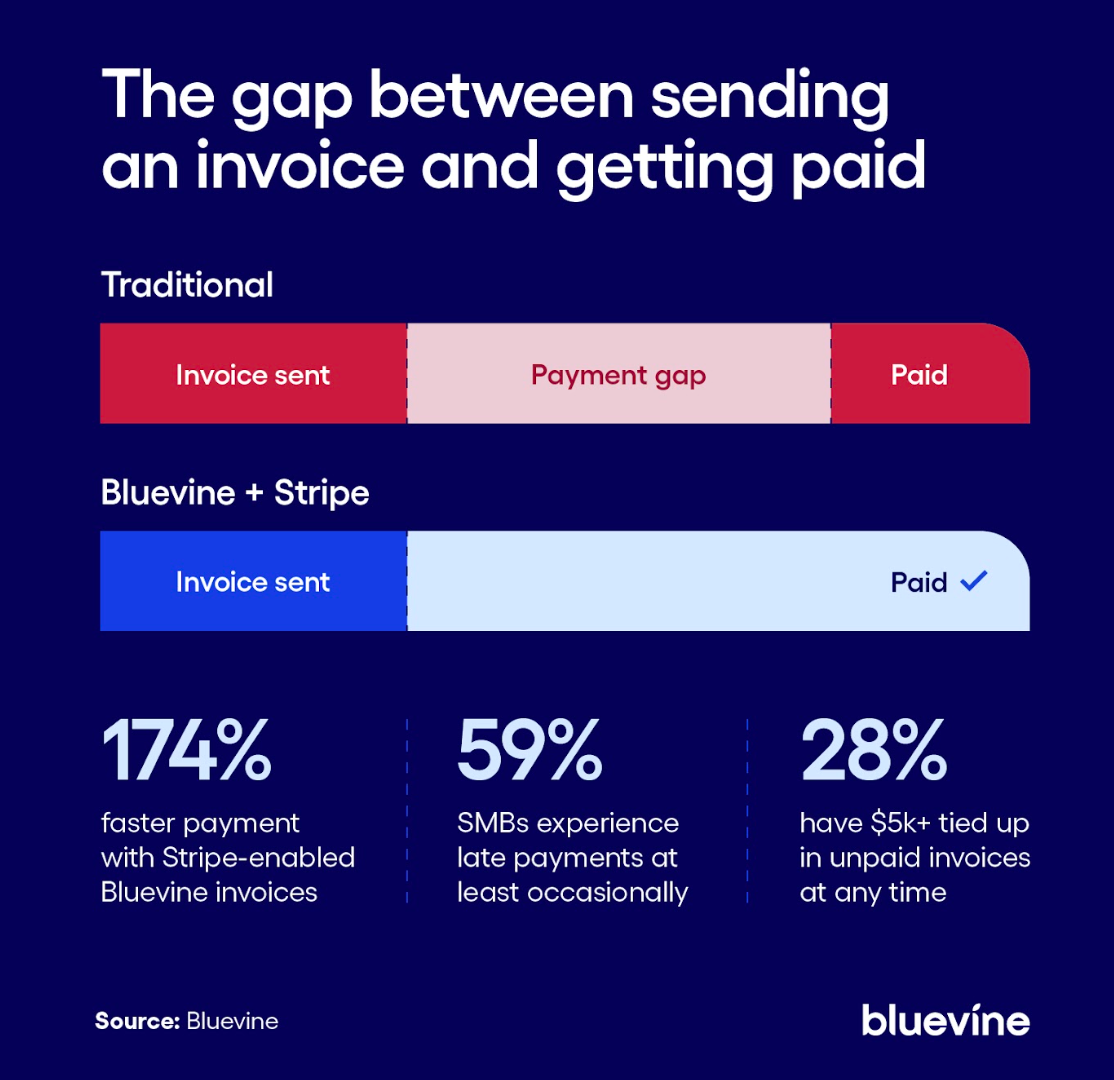

Stripe-enabled Bluevine invoices are paid nearly 3x faster—being paid in 7 days vs. 18 days on average—showing how reducing payment friction directly impacts cash cycles.

59% of SMBs experience late payments—and 28% have $5K+ tied up

Late payments are common. Nearly 6 in 10 small businesses report at least occasional delays.

Even when invoices eventually clear, the gap between issuing an invoice and receiving funds creates uncertainty in day-to-day cash management.

That uncertainty translates directly into locked-up cash: 28% of SMBs report $5,000 or more tied up in unpaid invoices at any given time. For context, nearly half of respondents generate less than $100,000 in annual revenue, meaning a $5,000 delay can represent a meaningful share of annual revenue for many respondents.

The operational cost compounds the financial strain. Nearly 1 in 5 (18%) SMBs say their biggest challenge with past-due invoices is spending time chasing payments instead of running their business. When owners manually track receivables or repeatedly follow up, delays become a productivity constraint.

Simplifying how customers pay also reduces delays. Internal Bluevine data shows that Stripe-enabled Bluevine invoicesBVSUP-00180—featuring built-in digital payment options—are paid 174% faster than traditional invoice methods–averaging only 7 days to get paid versus 18. When paying requires fewer steps, invoices clear more quickly and cash flow stabilizes.

1 in 6 SMBs have missed or nearly missed payroll due to late payments

Late payments quickly move from accounting into payroll.

For small businesses, the stakes are immediate. Nearly 1 in 6 SMBs (17%) report missing payroll or nearly missing it due to late payments. For businesses with employees, delayed invoices do not stay confined to accounting—they can affect paychecks.

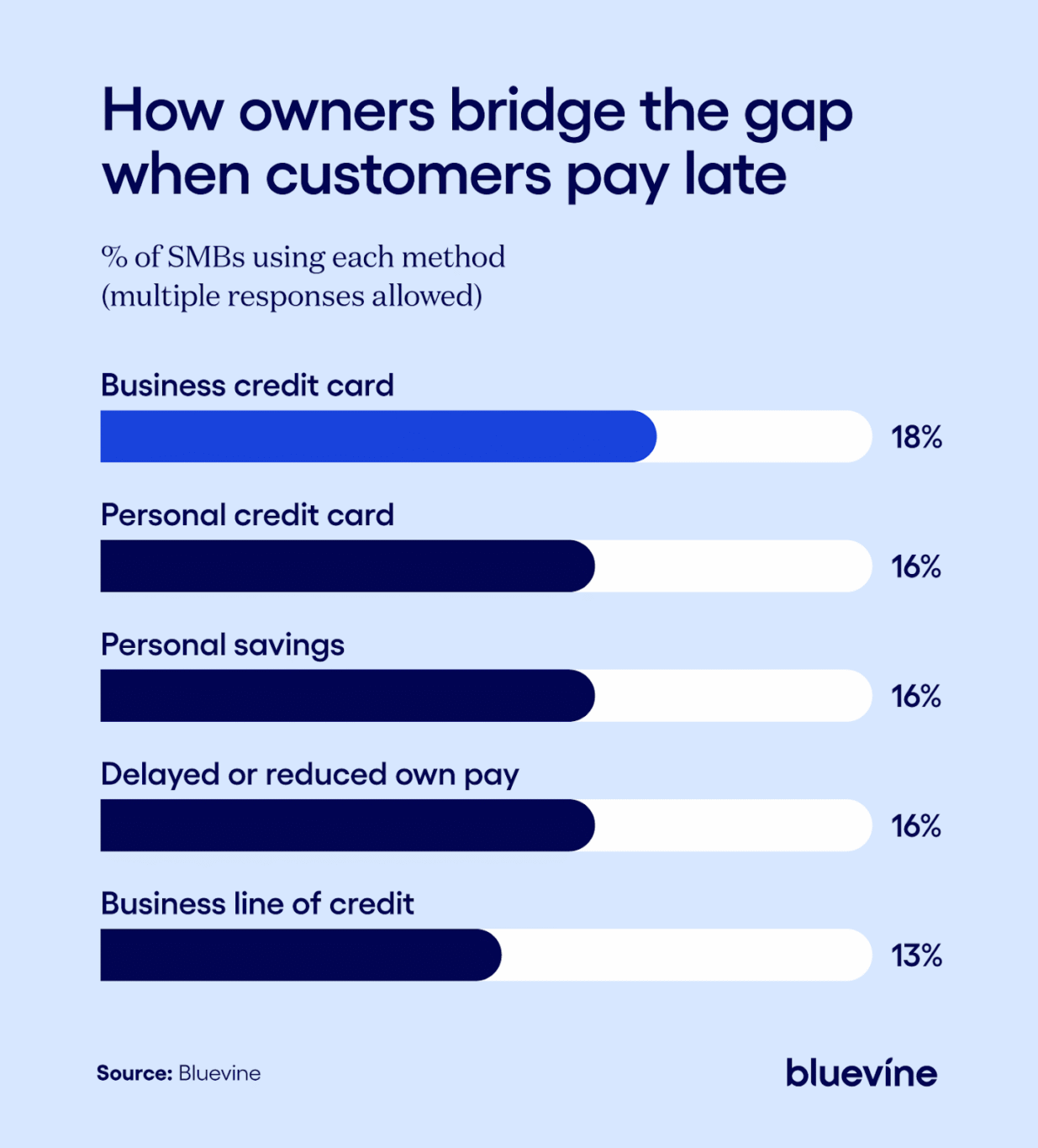

To bridge these gaps, many owners take on personal financial exposure. Rather than absorb a delay, many shift the burden onto credit or savings to keep operations moving.

Instead of generating profit, some owners finance operations out of pocket when customers pay late. Liquidity risk shifts from the customer to the business owner, putting an emotional toll on owners. 34% report increased stress or anxiety while waiting on overdue invoices, and 18% spend more time chasing payments than running the business. Late payments affect confidence and capacity—not just cash balances.

Only 31% keep a dedicated reserve for late payments—32% keep none

Small businesses are divided almost evenly between those prepared for payment delays and those operating without a buffer. Only 31% maintain a dedicated reserve specifically for late payments, while 32% keep none at all. This split underscores the uneven financial resilience across the SMB landscape.

Despite widespread lateness, only 19% charge late fees on overdue invoices, even though 59% experience some degree of late payment. Many businesses tolerate payment friction without formal guardrails, increasing exposure to recurring gaps.

For small business owners, using intelligent cash flow forecasting systems and interactive payment and invoicing tools can help minimize late payments and protect themselves from having to take drastic steps like cutting their own pay. For instance, at Bluevine we’ve seen that sending invoices with a payment gateway enabled get paid nearly three times faster than invoices without a payment option.”

– Kyle Cooper, SVP & GM of Bluevine Checking and Payments

At the same time, 46% report not experiencing cash-flow gaps due to slow payments. Resilience is possible—but it depends on whether systems are in place to absorb volatility before it escalates.

Building stronger reserves and improving visibility into financial inputs reduces volatility. Stronger cash flow management systems make uneven payment timing easier to absorb before it disrupts operations. Structural discipline reflected in small business cash flow—such as setting aside funds through sub-accounts and automated transfer rules, accepting faster digital payments directly to a Bluevine account through Stripe,BVSUP-00180 and aligning pricing expectations with estimates before work begins—creates the stability that distinguishes buffered firms from exposed ones.

The payment gap is a stability test for small businesses

Late payments have become a routine source of stress for many small businesses. The real question is whether a company can absorb the timing gap without jeopardizing its financial stability.

When owners delay paying themselves or rely on credit to keep operations moving, receivables timing becomes a structural risk. The divide between buffered and exposed firms highlights that financial resilience depends on visibility, discipline, and access to capital that smooths uneven cash cycles.

Financial resilience depends on tighter receivables processes, stronger reserves, and real-time visibility into financial inputs—before payment delays escalate into payroll or liquidity risks.

Late payments may remain part of doing business—but with stronger systems in place, they don’t need to define financial stability.

Bluevine’s comprehensive banking platform centralizes receivables, streamlines bill pay, and provides flexible capital designed to stabilize uneven cash cycles—helping owners maintain stronger cash flow control and make more confident financial decisions.

Join the largest small business banking platform in the U.S.BVSUP-00186

The survey was conducted by Centiment for Bluevine. The survey was fielded between February 2, 2026, and February 5, 2026. The results are based on 1,052 completed surveys. In order to qualify, respondents were screened to be residents of the United States, over 18 years of age, and a small business owner or professional. Data is unweighted, and the margin of error is approximately +/-3% for the overall sample with a 95% confidence level.

Disclaimer

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

Get answers in a snap, right from your dashboard during business hours.

Disclaimer

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

Subscribe to our monthly email newsletter.

Be the first to hear about Bluevine’s latest tips, insights, and product offerings.

Bluevine is a financial technology company, not a bank. Banking services provided by Coastal Community Bank, Member FDIC. Not all features available in all countries. Limitations apply. See international features for details.