Unstable sales, rising expenses, unpredictable payments: Today’s small business math rarely balances itself. For many, that adds up to a daily cash flow puzzle.

We surveyed 774 U.S. owners with $50K–$5M in annual revenue to see how they navigate cash flow and prepare for crunches, covering cash on hand, emergency triggers, access to funding, and the tools they are adopting.

Here’s what stood out—and how small businesses can tighten cash flow, build resilience, and stay ready for what’s next.

Key takeaways

Nearly 4 in 10 SMBs (39%) have less than one month’s worth of operating expenses on hand.

51.3% would tap emergency reserves within 48 hours to make payroll—before using them for upcoming taxes or deposits on unexpected large orders.

42.8% say access to cash matters more than returns—only 18.6% disagree.

Over two-thirds are interested in AI for cash flow management; “very interested” spikes to 54.26% in retail/ecommerce vs. just 17.6% in transportation/logistics.

Only 38% of firms with under $250K in annual revenue have a line of credit vs. 63.4% above $250K.

Among those seeking funds, 25.6% say funding was difficult to obtain, and 39.4% cite high interest rates as the top loan barrier.

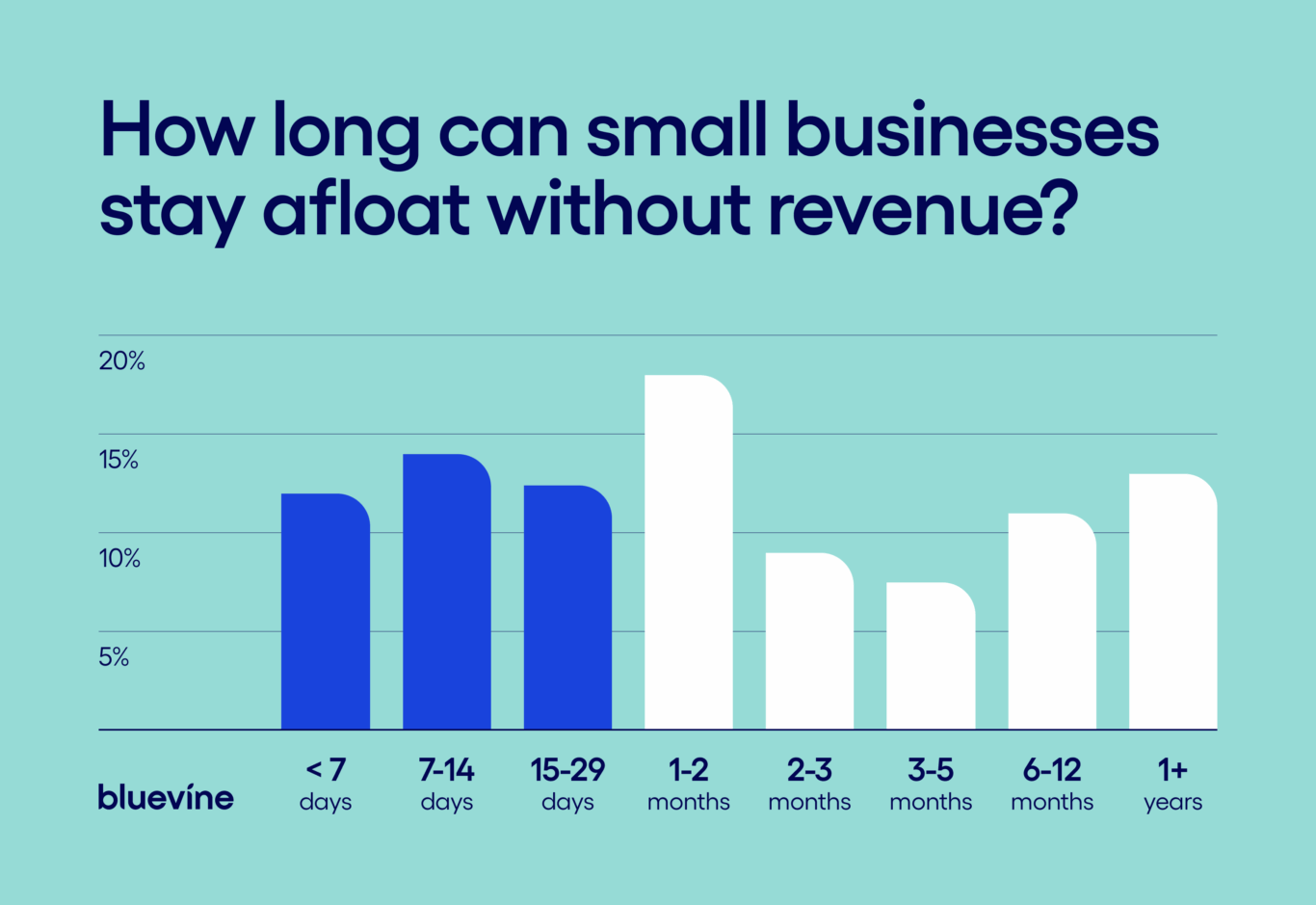

Nearly 4 in 10 businesses cannot cover more than a month of expenses

Most owners do not keep the kind of cash cushion they should—and that gap shows up fast when payroll, taxes, or a rush order hits. Our survey uncovered that nearly 4 in 10 small businesses (39%) cannot cover more than a month of expenses in the face of sudden financial disruptions.

Source: September 2025 SMB Survey, Bluevine/Centiment

Small business accountant, bookkeeper, and fractional CFO Eric Trettel recommends that most businesses keep at least 8–13 weeks’ worth of operating expenses in reserve. For context, JPMorgan Chase research has long flagged that most SMBs only have about 18 days of buffer.

Trettel says, “Businesses that collect receivables quickly can probably keep less if sales are forecasted to at least stay the same. However, any seasonal business, or businesses with long customer payment terms, should aim to keep additional funds to help cover expenses through periods with less revenue.“

Younger firms tend to be more exposed. In our study, only 19.6% of businesses 5 years old or younger carry 3–12 months of cash, compared with 39.2% of firms 6 years or older.

And the very youngest struggle most with day-to-day coverage: 20.7% of businesses under 2 years report less than seven days of cash in their checking account (versus 10.5% for those 11+ years). Solo operators face similar pressure because access to flexible financing is limited.

That fragility flows into funding. Just 21.4% of businesses less than a year old feel “very confident” about getting capital, compared to 43.7% of 11+ year firms. To bridge gaps, newer owners are more likely to reach for personal savings: 54% of 1-to-2-year businesses have used personal funds at least once, vs. 37.9% of firms 11+ years in.

The ultimate goal is to cover payroll, rent, and essential bills without relying on short-term borrowing. If the business is still growing or has unpredictable sales, build that reserve gradually by setting aside a percentage of monthly profits until you reach a comfortable cushion.”

– Eric Trettel, Founder of Sota Bookkeeping

How to start building business credit

If your business is new (up to 2 years old), prioritize building credit and banking relationships now by doing the following:

Establish business credit: Get an Employer Identification Number (EIN), separate personal/business finances, pay vendors on time, and monitor your business credit scores.

Open dedicated accounts: Use a business checking account for all revenue and expenses to create a clean financial history.

Secure a modest line of credit early: Apply while cash flow is stable so funds are available before you need them.

Formalize banking relationships: Connect with a representative from your banking platform, discuss products (LOC, overdraft, treasury tools), and keep docs up-to-date for faster approvals.

Reduce reliance on personal funds: Set a target reserve of three to six months of operating expenses and automate transfers to build it.

Half of business owners would tap into reserves if payroll were at risk

Emergency triggers show what keeps owners up at night. Payroll comes first—because missing a payday risks legal action, back-pay claims, and employee trust.

In our survey, 51.3% of owners said they would move money from emergency funds within 48 hours to make payroll.

Beyond team morale, federal rules require timely, full payment for hours worked. Failure to do so can lead to back wages plus liquidated damages under the Fair Labor Standards Act (FLSA), and state laws often add additional penalties.

Taxes are next: 40.4% said an upcoming tax deadline would prompt action, which tracks with IRS failure to deposit penalties for late employment tax deposits. And 36.4% would act if a large, unexpected order required a deposit, choosing to protect revenue momentum even if it means tapping reserves.

Industry patterns matter here, too. Retail/ecommerce respondents were nearly twice as likely to dip into reserves for supplier discounts (25.5%) than those operating in professional/business services (13.8%).

Early payment terms like 2/10 net 30 effectively offer double-digit annualized returns for paying suppliers sooner—valuable if the cash to do so is available.

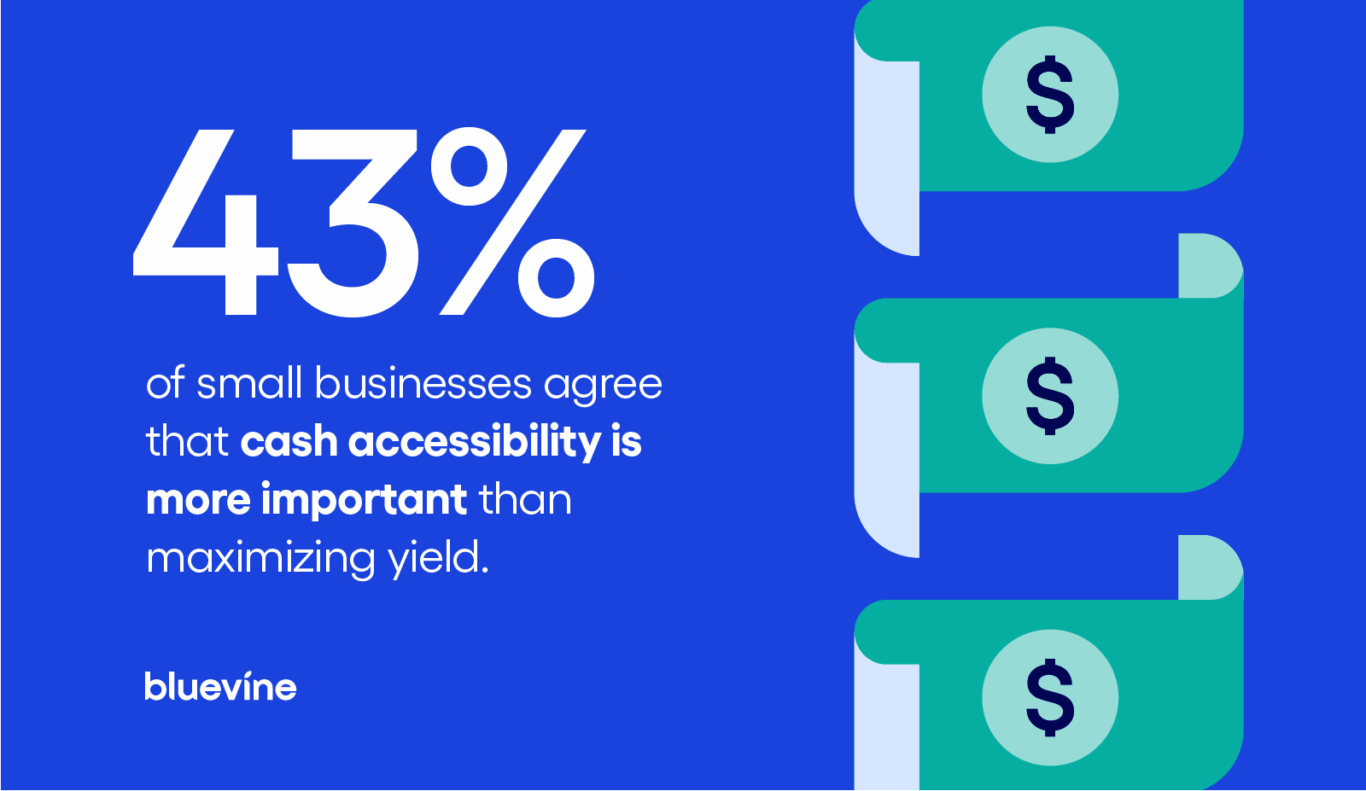

42.8% of small businesses keep money liquid, even if it means lower returns

Owners are still favoring reach-for-it-now cash over higher-yield options. In our survey, 42.8% agreed that access to cash matters more than maximizing returns, while 18.6% disagreed.

Source: September 2025 SMB Survey, Bluevine/Centiment

That tilt toward liquidity fits the moment. Pandemic-era shocks showed how quickly cash needs can change and how thin buffers can be, a lesson echoed by recent findings on small businesses in distress.

Our research on would-be business founders shows people favor fast payment processing/funds availability and easy access to credit/loans over high-interest accounts—signals that liquidity and working capital outrank rate-chasing when money needs to move quickly.

Caution is also showing up in sentiment data. The National Small Business Association’s latest report highlights economic uncertainty as the top challenge for owners. Nearly 60% say it is their biggest hurdle, the highest in 13 years—which makes keeping cash flexible feel safer than chasing yield.

When demand is uneven or policies are in flux, liquidity buys time to make payroll, cover taxes, and capture urgent orders without scrambling for financing.

Did you know?

You don’t need to choose between liquidity and annual percentage yield (APY)—you can have both.

Over two-thirds of businesses are interested in AI finance tools

Owners are leaning into AI for day-to-day finance work like cash flow forecasting, invoice handling, and faster collections. In our survey, 67.9% of businesses said they are interested in AI tools for cash flow management, and only 13% are opposed. Interest is broad across company ages, suggesting AI is moving from “nice to have” to standard tooling.

There is a particularly sharp divide among industries:

In retail/ecommerce, 54.26% of respondents reported being very interested in AI finance tools.

In technology/SaaS, 44.8% of respondents said they are very interested.

In transportation/logistics, only 17.6% of respondents selected “very interested.”

Together, these results suggest that AI finance interest runs higher in transaction-heavy sectors like retail/ecommerce and tech, and lower in logistics, where the payback is less immediate.

Many SMBs are already embracing the AI evolution. A recent Intuit QuickBooks survey of 2,200 U.S. small businesses found that 68% now use AI regularly, up from 48% in 2024. In finance specifically, common applications include AP/AR automation—OCR and machine learning that read invoices, route approvals, and predict late payments.

Close bills faster with fewer clicks, more payment options, and AP automation tools.

Less than 40% of businesses making $250K or less have credit lines in case of emergencies

Higher-revenue businesses are better prepared for shocks—and they tend to act faster when rates move.

In our survey, 63.4% of firms earning >$250K per year keep a line of credit (LOC) for emergencies vs. just 38% of firms earning <$250K.

Smaller firms also have less capacity to absorb big gaps: Only 7.7% of businesses <$250K could cover a $100K shortfall, compared to 61.3% of firms $1M+.

Refinancing behavior in our survey aligns with this access gap. If rates drop, 45.5% of companies making >$1M say they would refinance debt, compared to 33% of firms earning <$250K.

The top reason smaller firms would not refinance was simple: “I don’t have any business debt” (44.8%). This was consistent with lower LOC usage among sub-$250K businesses (38%).

In short, more revenue generally means more credit tools and more ways to respond quickly to changing conditions.

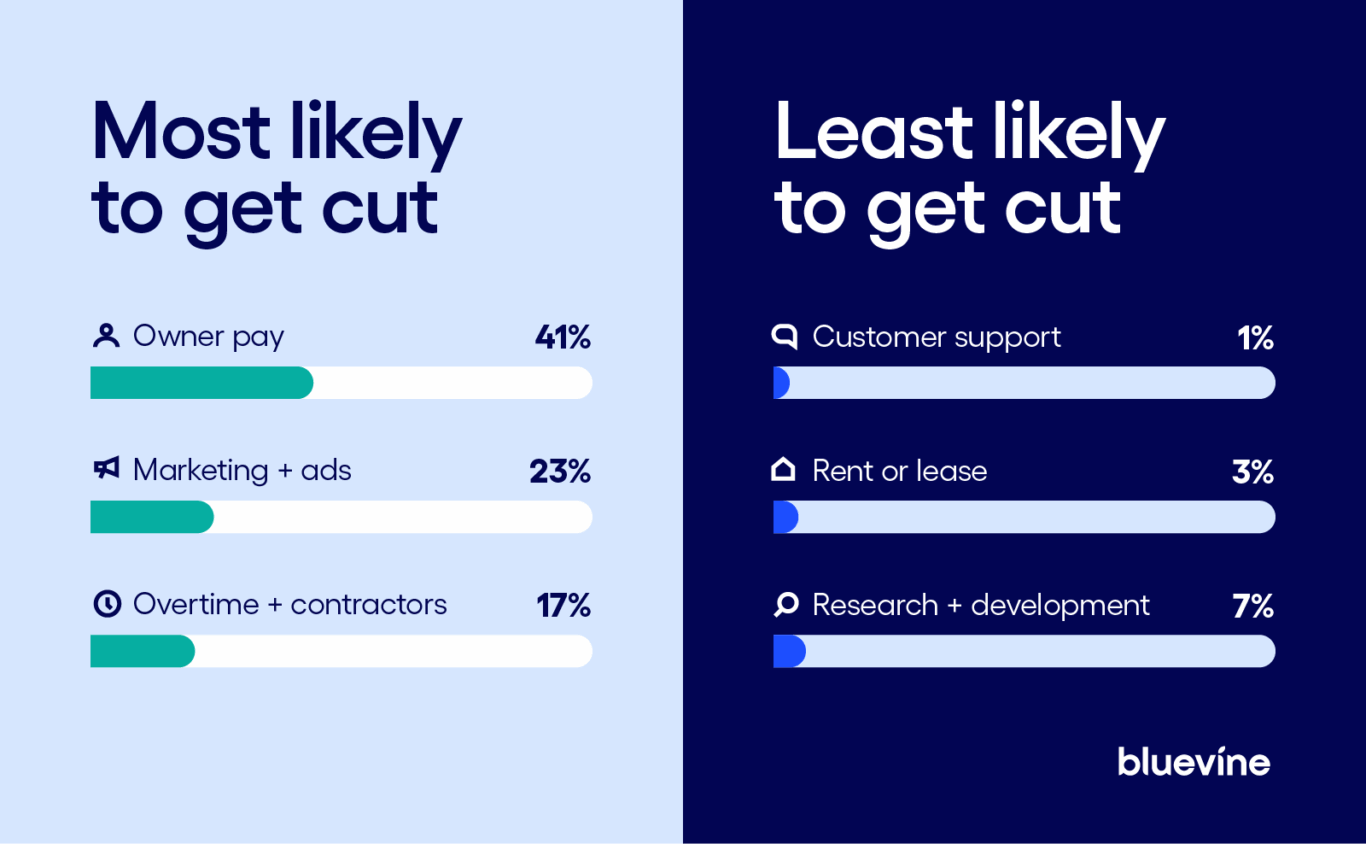

41% of business owners would cut their pay before anything else in a cash crunch

Source: September 2025 SMB Survey, Bluevine/Centiment

In difficult economic times, it is usually the owners who take the first hit.

Michelle Blakemore, founder of BeMore Accounting & Consulting, recommends cutting your own salary “only after your reserves dip below 1–2 months of runway and you’ve exhausted every other lever—i.e., slashing non-essential costs, chasing overdue invoices, tapping short-term financing.” She adds, “I’d advise a 20–50% cut as a last resort, paired with clear parameters like this will last 90 days or until revenue rebounds. Remember: Your business needs your sharp mind more than your full paycheck, so protect that first.”

See why Michelle recommends Bluevine to her SMB clients.

Our survey revealed that the first move owners would make when money gets tight was to cut their own pay (41.1%).

The next lever was marketing/ad spend (22.9%), showing how quickly discretionary budgets get trimmed.

Only a tiny share would start with customer support/client services (1.4%), underscoring how important service is to retention and revenue.

We also discovered that team size plays a role in deciding what to cut:

Larger teams cut owner pay first more often:73% of firms with 250+ employees would reduce owner pay in a crunch, versus 52% of solopreneurs.

Bigger firms have more levers to pull: Companies with 10+ employees are more likely to cut overtime or contractors first (23.4%) than solopreneurs (10.1%).

For these reasons, many experts recommend applying for financing when your business finances are healthy—so funds are available when cash gets tight.

Eric Trettel, owner of Sota Bookkeeping, says: “The best time to secure financing is before you actually need it. Consider applying for a line of credit right after tax season or during a strong quarter, when your financial statements best represent the business’s stability.”

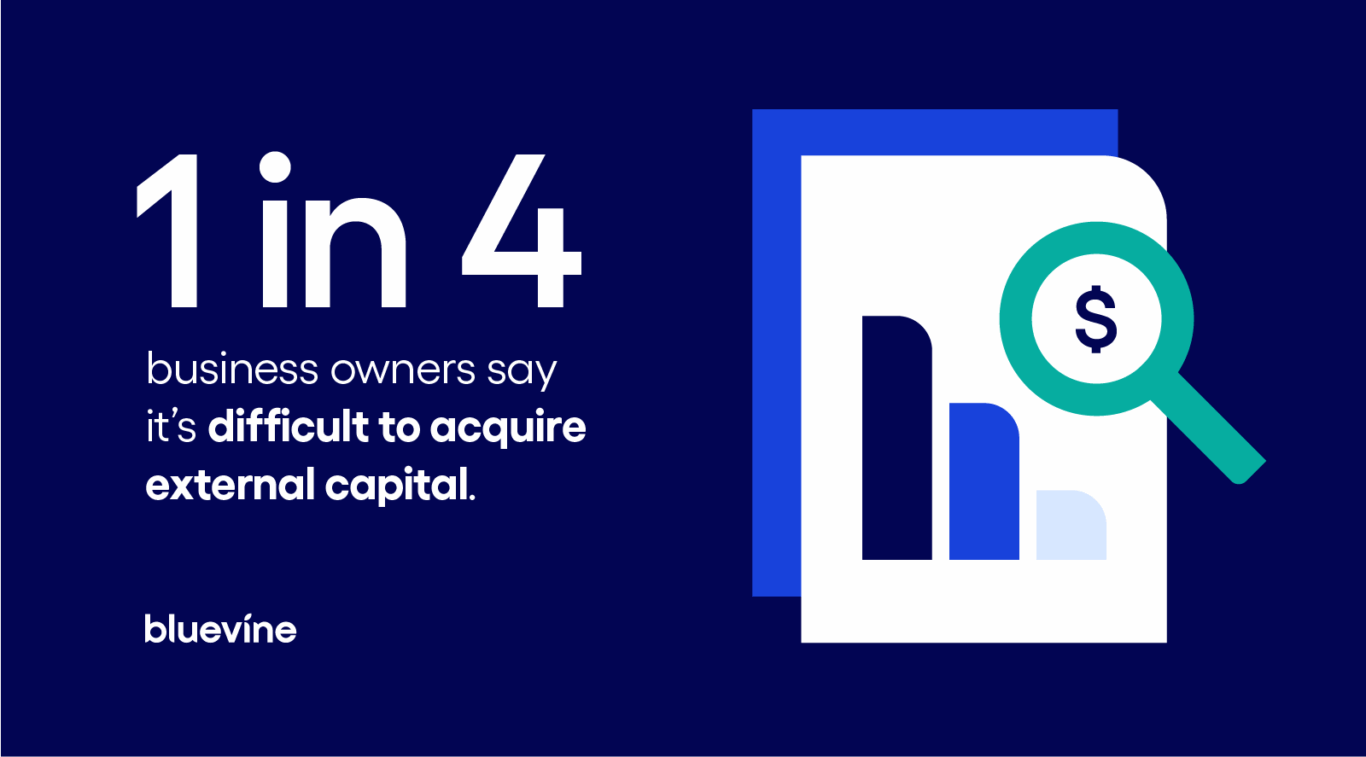

A quarter of business owners say it is difficult to acquire external capital

Source: September 2025 SMB Survey, Bluevine/Centiment

Owners are looking for funding, but according to our survey, that is easier said than done. Of the 68.2% of owners seeking external capital in the past 12 months, 1 in 4 applicants (25.6%) said it was difficult to obtain.

The biggest pain points were:

Low credit scores (8.1%)

Limited operating history / thin credit files (6%)

Unclear decisions during underwriting (5.9%)

This tracks with industry trends: The Federal Reserve reports that application rates held steady in 2024 while approval satisfaction fell.

Many owners avoid new loans for two simple reasons:

They do not want to add debt(31.4%): Debt aversion skews toward smaller companies—84% of those who chose “don’t want more debt” have fewer than 25 employees.

Total cost is unclear (fees, APR, prepayment penalties) (15.6%): This pricing issue is concentrated at larger firms (45% of 100+ employee companies vs. 13% of companies with fewer than 25 employees).

Recent policy moves aim to improve clarity. The CFPB’s Section 1071 data collection rule (now moving forward after court challenges) will require lenders to collect and report standardized data on small business credit applications, which should make pricing and approval criteria more transparent and comparable for owners.

Roughly 40% of small business owners cite high interest rates as the top loan barrier

Owners are watching rates, and even after the Fed’s September quarter-point cut, most plan to hold off on new hires or big marketing pushes until conditions feel steadier.

In fact, 39.4% cited “rates are still too high” as their biggest barrier to asking for a business loan right now.

In our data, the top-cited moves if rates fall are still building emergency reserves (21.3%) and paying down principal (21.1%), with far fewer planning to ramp marketing (13.8%), hire (3.4%), or accelerate holiday spend (5%).

The Fed’s minutes also signaled support for further rate cuts, but businesses appear to be waiting for clearer conditions before shifting from balance-sheet repair to growth.

How owners would use savings if rates drop also varies by size:

21% of $1M+ businesses say they would pay down principal faster; in the $250K-$999K band, that rises to 23.3%.

For the smallest firms (<$250K), the priority is to build an emergency reserve (21.9%)—a smart move when liquidity cushions are thin.

Put liquidity first with business checking

The picture is clear: Many owners are operating with thin buffers, prioritizing access to cash over yield, and staying conservative about new borrowing. When conditions shift, businesses with the right accounts, credit tools, and workflows already in place are the ones that move first.

Bluevine can help owners turn that caution into control. The Bluevine Business Checking account centralizes inflows and outflows so cash stays accessible when payroll, taxes, or rush orders hit. Pair it with a line of credit for flexible working capital—draw what you need, repay, and redraw without over-borrowing. Plus, access your approved line of credit draws instantly in your Bluevine checking account.BVSUP-00127

Make your cash work harder: Reduce fees, protect deposits, and earn higher interest on checking balances.

Centiment Audience conducted this survey of 774 U.S. business owners with $50K–$5M in annual revenue for Bluevine between September 25 and September 30, 2025. Data is unweighted, and the margin of error is approximately +/-3% for the overall sample with a 95% confidence level.

Disclaimer

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

Get answers in a snap, right from your dashboard during business hours.

Disclaimer

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

Subscribe to our monthly email newsletter.

Be the first to hear about Bluevine’s latest tips, insights, and product offerings.

Bluevine is a financial technology company, not a bank. Banking services provided by Coastal Community Bank, Member FDIC. Not all features available in all countries. Limitations apply. See international features for details.