Having extra cash on hand is crucial for businesses of all sizes—whether you’re looking to expand operations, cover an unexpected cash flow gap, or capitalize on a seasonal opportunity, a business line of credit is a reliable, long-term way to get that cash when you need it.

Business lines of credit are one of the most popular choices among business owners who apply for financing, but how easy is it to actually get one? Our survey shows that only 38% of firms with annual revenue under $250,000 have a business line of credit. Comparing this to the 63% of those above that threshold highlights how smaller businesses often struggle to qualify.

Your chances of getting approved mostly depend on just a few factors. Most lenders require you to be in business for at least one to two years and present a strong business credit profile. Larger or lower-interest lines of credit will have stricter conditions and may require collateral.

This may seem daunting, especially if you’re a startup that needs a line of credit. Thankfully, applying online has never been easier—we’ve laid out five straightforward steps for how to get a line of credit for your business.

What you need to know

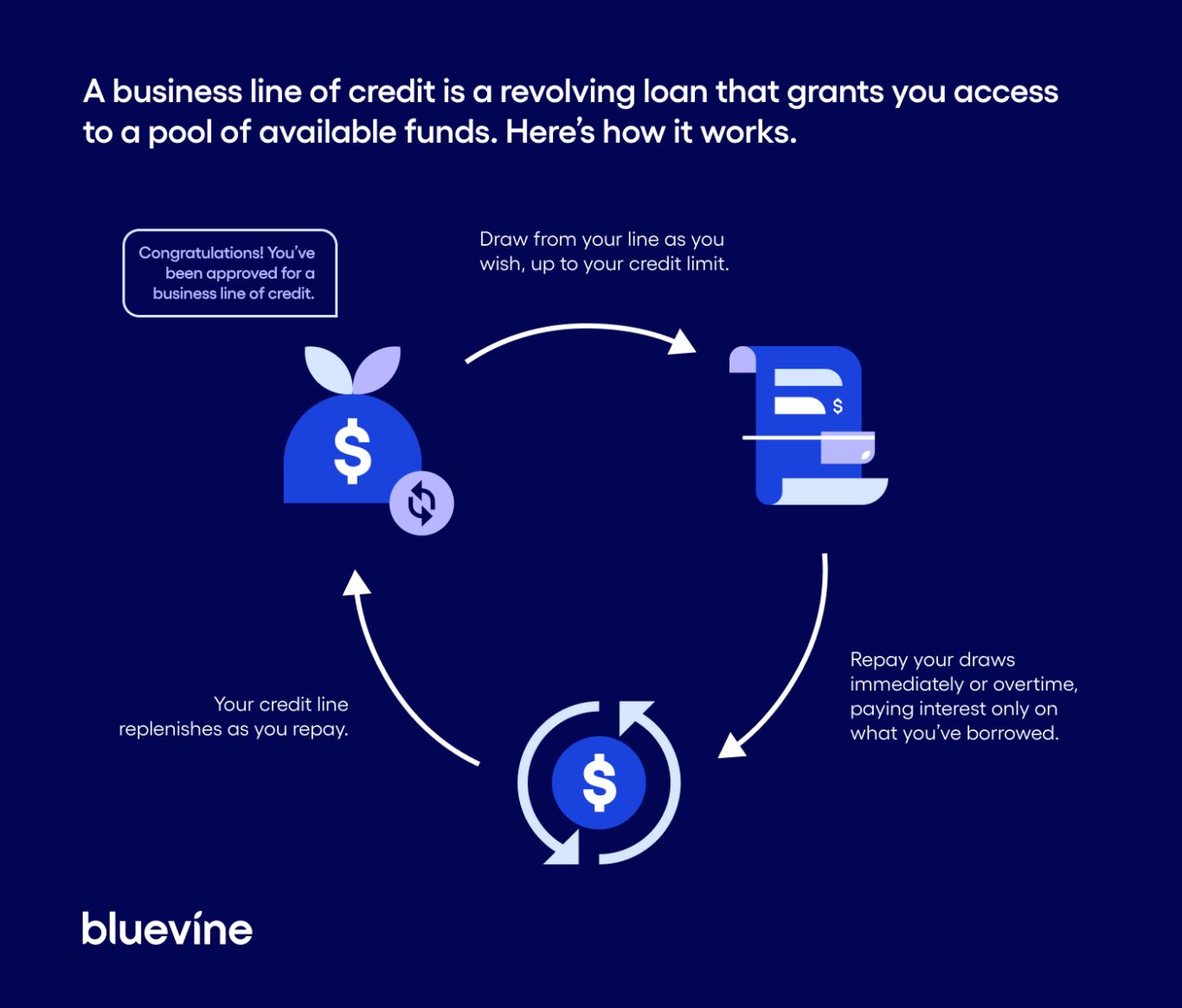

- A business line of credit is a pool of funds that replenishes as you repay your draws.

- They’re a flexible, affordable form of debt financing for covering ongoing expenses such as rent, payroll, or inventory, or for taking on new projects or expansion opportunities.

- To apply, review your finances, research different types of lenders and loans, and apply online. If a line of credit isn’t right for you, consider a term loan or SBA loan.

How does a line of credit work?

Secured versus unsecured business lines of credit

If you’re an established business with a strong credit profile, you may face a choice between a secured or unsecured line of credit.

- Secured lines of credit require you to post collateral, like property or ownership equity, which you agree to forfeit if you can’t repay the loan. Because the risk to lenders is lower, you’ll receive more favorable terms, like a higher credit limit and lower interest rate.

- Unsecured lines of credit don’t require you to post collateral, so the risk to you is much lower. Because the risk to lenders is higher, you’ll receive slightly less favorable terms, like a lower credit limit and higher interest rate.

Do you need a business line of credit?

A business line of credit is a uniquely flexible form of financing for businesses to cover expenses and finance growth opportunities at every stage of business growth. They’re also more affordable than other types of debt-based financing—interest rates are low, and you only pay interest on the amount you draw.

If you need funds to pay rent, cover payroll, purchase equipment, or take on a new project, a business line of credit offers flexible, affordable access to working capital. Many small businesses lack the cash reserves to cover large expenses. Just 8% of companies earning under $250,000 annually could cover a $100,000 emergency from cash alone—compared to 61% of businesses making $1 million or more. A business line of credit gives you a crucial financial buffer, so you’re ready when the unexpected happens.

How to apply for a business line of credit

You’ve assessed your business needs and determined that a line of credit would boost your growth. What’s next?

1. Review your credit score and finances

Most lenders have similar minimum requirements. To see if you’re qualified for a business line of credit, make sure the following applies to your business:

- 625+ FICO score

- In business for 2+ years

- No bankruptcies for the past three years

- Strong business credit profile. Lenders will look at your personal and business credit scores to gauge the creditworthiness of your business. The stronger your scores, the more options you have. You can build business credit by making consistent, on-time payments on recurring bills and debts.

- $40,000 in monthly/annual revenue. To determine whether you can pay back your credit line, lenders will forecast your cash flow based on your monthly statements. Lenders also want to see consistent annual growth, so they can increase your credit line as you grow your business.

If your business doesn’t meet all these benchmarks, you might still find options. Some alternative lenders accept newer businesses (as little as 6–12 months old or with lower revenues) in exchange for higher interest rates or collateral.

2. Compare your options

Once you’ve confirmed that you qualify for a business line of credit, your next step is to understand the pros and cons of each type of lender.

- Traditional bank lines of credit offer favorable terms and low interest rates, but also have stricter requirements and thorough applications. Contact any banks you have an existing relationship with to see if you qualify.

- Online lenders offer shorter applications, more lenient requirements, and faster approval, but with slightly higher interest rates. Online lenders are generally the most accessible, requiring only a phone or computer for all financial services and 24/7 access.

- Credit unions are member-owned and non-profit, which means lower rates and favorable terms for lending customers who join, but also fewer branches than traditional banks. Some credit unions are community-based, which requires you to live within a certain area, and others are occupation-based.

3. Gather required documents and submit your application

While hunting for business lines of credit to apply for, compare terms, rates, and requirements across different types of lenders. Once you’ve chosen a few potential lenders, gather your documents so you can fill out your application in one sitting. It’s important that you only submit one application at a time (decisions are almost always made within a few days) and don’t open more than one credit line.

Here are some of the documents and information you’ll be expected to submit to a lender:

- Personal information: To verify your identity, lenders will require you to submit information about yourself. This includes your full legal name, Social Security number, criminal record, and educational background.

- Bank statements: Many lenders require at least one year of bank statements.

- Financial statements: To determine the financial strength of your business, you’ll need to submit documents such as your profit and loss sheet, cash flow sheet, and balance sheet.

- Information about other stakeholders: If you own less than 50% of the business, you must provide information about any additional stakeholders.

- Legal documents: Depending on the lender you apply to, you’ll be expected to submit one or more of the following: business licenses and registrations, articles of incorporation, business tax ID, contracts with third parties and/or UCC filings.

- Debt schedule: If you have any existing debt, some lenders will expect you to provide a debt schedule. This shows all your business’s outstanding loans, credit, and payment schedule.

- Tax returns: Lenders will require you to show personal and business income tax returns over the last three years.

Once you’ve prepared all your documents, complete the lender’s application online (or in person if no online option is available). Some lenders conduct a hard credit inquiry that could briefly affect your credit score. Many online lenders can also verify your financial information digitally by letting you link your business bank account, which can speed up approval and reduce the paperwork you need to upload.

4. Review the offer and negotiate terms

Your application is unlikely to get rejected if your business meets all the lender requirements. Once approved, review the terms of the credit line offer, such as your credit limit, whether your interest rates are fixed or variable, fees, repayment schedule, and any late payment penalties. Before accepting, negotiate terms so your line of credit can best benefit your business, particularly if you have above-average financials or competitive offers from other lenders.

Be sure to calculate the offer’s effective annual percentage rate (APR), including any fees so that you can compare the true yearly cost of different offers. If the interest rate is variable, ask whether there’s a cap or whether you can switch to a fixed rate later to avoid surprises in your payments.

5. Know the total cost of interest and fees

There are many different fees associated with a business line of credit. It’s important to understand the full amount you’ll be paying to the lender to avoid costly impacts to revenue or late payments. To start, your simple interest rate is the interest you’ll pay on top of the amount you borrow. So if you draw $10,000 with a 1% simple interest rate, you’ll repay $10,000 plus $100 in interest.

Here are some of the most common fees that lenders charge to use a business line of credit:

- Draw fees: charged on each draw you make, typically between 1–2% of the draw amount.

- Late fees: charged if you fail to make a payment on time (often a flat $20–$50).

- Maintenance fees: a monthly fee to cover the lender’s cost of keeping your credit line open.

- Annual fees: flat fees charged annually (sometimes in lieu of monthly maintenance).

- Prepayment fees: charged if you pay your balance off early (usually 3–5% of the amount). Most online lenders don’t charge prepayment fees.

- Origination fees: a one-time fee when the line of credit is opened.

Apply for a Bluevine Line of Credit in minutes to get financing that’s tailored to your business needs.

Avoid common line of credit application mistakes

Know why you need the funds

Lenders want to see that their financing fits into a long-term growth strategy for your business. When applying for a business line of credit, come prepared with a plan that demonstrates how you’ll use the funds. Forecast your cash flow and the returns from any investments to help choose the right loan size.

For example, if you plan to use the credit line to purchase extra inventory for a holiday season rush, prepare a sales projection and repayment plan to show how you’ll pay it back after the season.

Don’t take out more than one business line of credit (also known as loan stacking), and don’t draw more than you can afford to pay back. When you consistently make repayments on-time, your business credit profile will improve, and you’ll be eligible for larger credit lines and other business loans.

Get help understanding the application

Small business owners wear many hats. In an emergency situation, it may be tempting to rush through as many credit line applications as possible, but this can hurt your chance to obtain financing. From typos in your information to misunderstanding different rates and fees, simple errors can cause large problems. Hire an accountant or bookkeeper to help compare line of credit terms.

Need accounting help?

Bluevine partners with a network of accountants and bookkeepers who specialize in small business finances. Browse our directory here.

Be honest

You may be tempted to understate any financial problems on your application, but this is a bad idea. Lenders read business plans and assess lending risk professionally—they understand that sometimes businesses require outside funding to grow, and how much debt is too much for your company to handle. They will also find out through their underwriting process whether you’ve misrepresented your finances, which will damage your chances of getting approved.

Business line of credit alternatives

If you don’t qualify for a business line of credit, or your business needs call for a different type of debt financing, you can try the options below:

- Term loans: A lump sum of funds paid upfront and repaid in fixed monthly installments over a set period (typically 3–6 years). They can be secured or unsecured. Term loans are ideal for projects that require a large amount of cash upfront, whereas lines of credit are better suited to ongoing or fluctuating funding needs.

- SBA loans: Unsecured loans administered through the U.S. Small Business Administration, ranging up to $5 million. You apply by entering your information on the SBA website, where you’ll be matched with one of the SBA’s partner lenders. These loans can take longer to get approved, but they offer low rates and long terms.

- Business credit cards: Credit cards issued to your company instead of to you personally. Business credit cards offer an easy way to separate business spending and earn cash back and other rewards—plus all fees, finance charges, and interest paid are tax-deductible. Many business credit card issuers also allow you to get additional employee cards, so you don’t have to exchange physical cards to make purchases.

Business line of credit FAQs

A secured line of credit requires collateral—private property or assets which you agree to forfeit if you can’t repay the credit line. Because the risk to the lender is lower, you can usually access much higher credit limits at lower interest rates, all while meeting lower requirements. As long as your business is able to repay the balance, secured lines of credit are a great way to quickly access capital. Mortgages and auto loans are common examples of secured loans.

An unsecured line of credit doesn’t require collateral. Because the risk to the lender is higher, you usually need to meet higher requirements for a smaller credit line and higher interest rates. If you don’t have collateral to offer or just want a less risky line, an unsecured line of credit is the safer option. Examples of unsecured credit or loans include credit cards and student loans.

A line of credit isn’t necessarily better than a term loan, but its flexibility may be a better fit for your business needs.

With a term loan, you receive a lump sum of funds and must start repaying the entire amount (plus interest) immediately. With a business line of credit, you’re only responsible for repaying what you’ve borrowed, not the entire credit limit. Plus, as you make repayments, your available credit replenishes, allowing you to borrow more funds. Conversely, a term loan can’t access additional funds until you’ve repaid the original loan.

When you apply for your line of credit, you’ll need to provide documentation that you meet each of these requirements:

625+ FICO score

In business for 2+ years

$40,000 in monthly revenue

In good standing

No bankruptcies for the past three years

You can apply for a line of credit as an LLC as long as you’ve established a solid business credit profile—for example, a 625+ FICO score, being in business for at least two years, in good standing with creditors, and with no recent bankruptcies in the past three years, and earning $40,000 or more in monthly revenue.

Next, you’ll need to gather the necessary documentation for the application—this includes official documents with basic information about you and your business, and a bank connection or bank statements for the past three months to one year.

It’s very difficult to get a true business line of credit until you’ve established your business credit profile. However, you may be able to apply for a personal line of credit, an SBA microloan, or a business credit card to fund the early stages of your business until you can qualify for a business line of credit.

With a term loan, you’ll receive a lump sum of money up front that you have to pay back over time. A line of credit is a long-term pot of money, which you can take from whenever you want (up to your credit limit) and replenishes as you repay what you took (plus interest).

Term loans are useful for specific projects that need an upfront investment, while a business line of credit is more flexible and cost-effective—you’ll pay less in interest for quicker access to funds.

A line of credit also better equips your business to handle periodic dips in sales or temporary emergencies without repeatedly applying for new loans. Some credit lines require approval for each draw, but they are much quicker than reapplying for a loan. Consistently repaying a line of credit will also help you build your business credit history.

If a revolving business line of credit isn’t right for you, there are other types of debt financing that may better suit your business needs.

For instance, term loans provide a lump sum you receive upfront and repay in fixed installments over several years. If you’re willing to post collateral, you may get approved for a larger secured term loan with a longer repayment period.

Another option is SBA loans, which are unsecured loans issued by the U.S. Small Business Administration, via its lending partners. These can offer up to $5 million in funding, often with favorable terms, though the application process is more involved.

Yes. Many traditional and virtually all online lenders offer online applications for business lines of credit. If you’ve prepared all your documents in advance, applying online should only take a few minutes. Generally, the process will follow these steps:

1. Go to your lender’s website and find the online application for a business line of credit.

2. Fill out the application and upload your documentation.

3. Once you’ve submitted an application, you should get a decision within one to two business days.

This article was originally published on Dec. 28, 2016. It was updated on November 22, 2024.