Many small businesses operate on a thin cash cushion, so one slow month can make it hard to cover rent, payroll, or other essential expenses.

According to a recent Bluevine survey, nearly 4 in 10 small businesses (39%) can’t cover more than a month of expenses. A cash flow statement can show you why that happens by breaking down exactly how cash enters and leaves your business.

In this guide, we’ll break down what a cash flow statement is, the sections it includes, and how to prepare one. We’ll also walk through a simple example you can adapt for your own business.

What you need to know

- A cash flow statement shows how cash actually moves in and out of your business, so you can see if you can cover short-term expenses.

- The three sections (operating, investing, and financing) work together to explain what’s really driving your cash position.

- Reviewing cash flow statement examples can help you identify when you might need tools like a line of credit to fill financial gaps.

What is a cash flow statement?

A cash flow statement is a financial report that shows how cash moves in and out of your business over a set period. It’s the clearest way to measure liquidity and understand whether your business has enough cash on hand to cover expenses, payroll, and upcoming obligations.

Cash flow statement vs. income statement

The income statement and cash flow statement are easy to confuse—both summarize financial activity over a period, but they measure different things.

- An income statement shows revenue, expenses, and profit based on when they’re earned or incurred—even if the money hasn’t moved yet.

- A cash flow statement shows actual cash in and out of the business.

For example, you might record $10,000 in sales on your income statement for the month, but if customers haven’t paid yet, your cash flow statement will show $0 in cash received. This gap explains why businesses can appear profitable on paper while struggling to pay their bills in reality.

Bluevine Tip

One of the most common payroll mistakes small businesses make is misclassifying workers. Be sure to correctly categorize full-time employees and independent contractors—as well as exempt and non-exempt employees—to avoid lawsuits and fines from the IRS.

The 3 key elements of a cash flow statement

A cash flow statement is divided into three sections that show where cash is coming from and where it’s going. Together, they help you understand both daily operations and longer-term financial decisions.

Operating activities cover cash generated or used by your day-to-day business—customer payments, supplier costs, payroll, rent, and other routine expenses.

- What it shows: Whether your core operations reliably produce enough cash to sustain the business.

Investing activities track cash spent on long-term assets like equipment, vehicles, or software, as well as cash received from selling those assets.

- What it shows: How much you’re reinvesting in the business and how those purchases affect available cash in the short term.

Financing activities reflect how the business raises or returns capital, including loan proceeds, repayments, owner contributions, or distributions.

- What it shows: How debt and equity decisions impact your liquidity and financial flexibility.

Did you know?

Bluevine Business Checking gives you a variety of easy ways to get paid, including built-in invoicing tools and Tap to Pay functionality that allow you to accept credit cards and digital wallet payments online and in person.

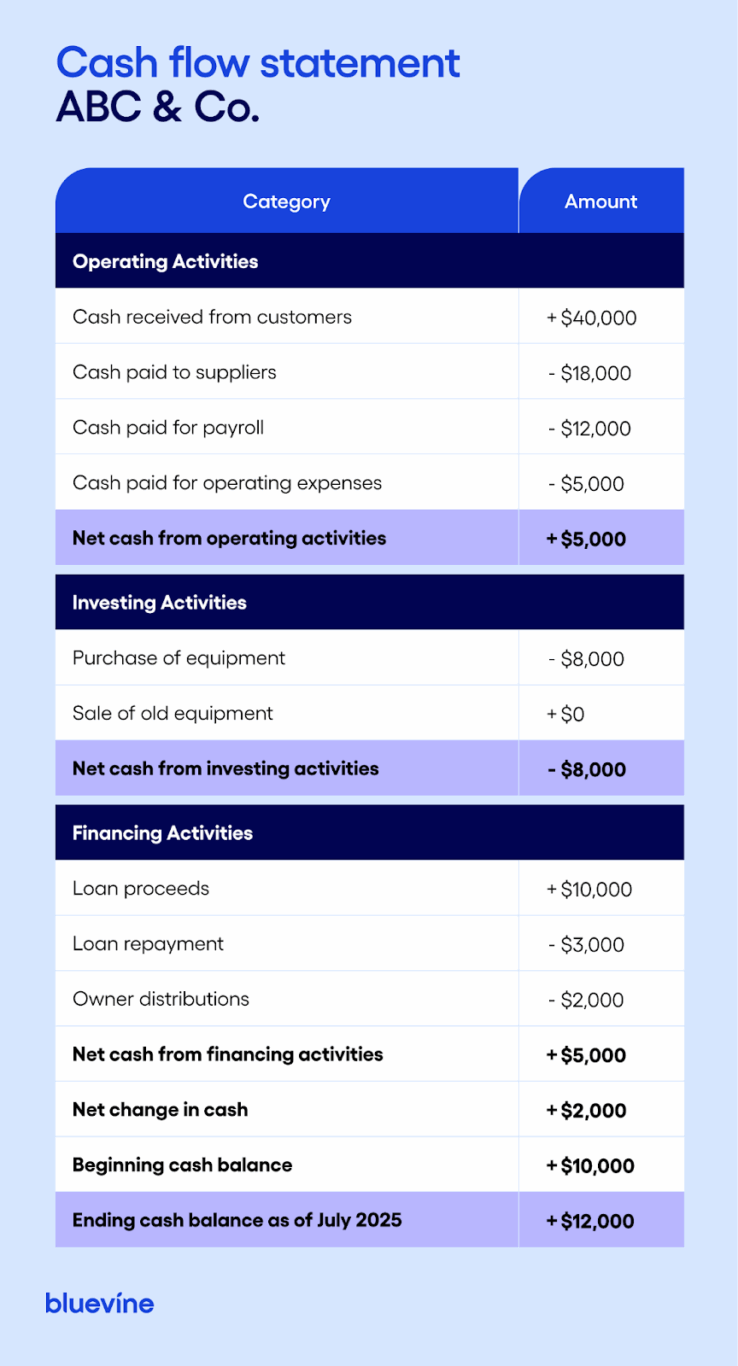

Cash flow statement example

Below is a sample cash flow statement format for a fictional small business, showing one month of activity. This hypothetical example mirrors what you’ll see in basic financial reporting.

Click here to download an editable PDF of this template that you can use for your own business.

Why are cash flow statements important?

A cash flow statement helps you gauge your financial stability, which helps you manage your money better and make decisions based on real liquidity, not just profit. Let’s look at some main benefits of a cash flow statement:

- Analyzing financial flexibility: Shows whether your business can handle a setback without outside funding and whether you have enough cash strength to act on growth opportunities when they arise.

- Assessing liquidity: Helps you see if you can cover short-term obligations like payroll, rent, taxes, and vendor payments without delays or borrowing.

- Forecasting cash flows: Provides the historical data you need to project future inflows and outflows so you can prepare for slow periods and plan large expenses.

- Performance assessment: Breaks down how operations, investments, and financing contribute to your cash position, helping you spot strong areas and areas that need attention.

- Revealing the full picture (vs. profit): Highlights that profit doesn’t always equal cash. Timing differences and non-cash expenses can mask real liquidity, making the cash flow statement a clearer indicator of what’s available to spend.

Methods for calculating a cash flow statement

There are two common ways to prepare a cash flow statement: the direct method and the indirect method. Both produce the same final cash flow total, but differ in how you’ll calculate cash flow from operating activities.

Direct method

The direct method lists the actual cash coming in and going out during the period. This includes cash received from a sale, cash paid to vendors, payroll, rent, and other operating expenses. It’s easy to understand because it shows real cash movements without adjustments.

This method is useful for smaller businesses or companies that want a clear view of day-to-day cash activity. The drawback is that you have to track every cash transaction, which can be slow and tedious if done manually.

Let’s use an example to understand this method better:

Your business receives $25,000 in cash from customers this month. You pay $8,000 to suppliers, $10,000 for payroll, and $2,000 for rent and utilities:

- Operating cash flow (direct) = $25,000 − $8,000 − $10,000 − $2,000 = $5,000

This method shows the exact cash coming in and going out, line by line.

Indirect method

The indirect method adjusts your net income to show what the cash involved in your transactions actually did. It adds back expenses that didn’t involve cash (like depreciation) and accounts for timing differences in things like unpaid bills or customer payments that haven’t come in yet. This method starts with profit and adjusts it to reflect actual cash movement.

This method is helpful for most small businesses because it’s quicker to prepare. You don’t have to track every cash movement—you just start with your profit and make a few adjustments.

Let’s see this method in action:

Say your net income was $7,000 for the month.

- Add back depreciation on equipment: + $1,000 (a non-cash expense)

- Adjust for a $3,000 increase in accounts receivable (customers haven’t paid yet): − $3,000

- Adjust for a $500 increase in accounts payable (you haven’t paid a vendor yet): + $500

- Operating cash flow (indirect) = $7,000 + $1,000 − $3,000 + $500 = $5,500

How to prepare a cash flow statement

Preparing a cash flow statement involves gathering your financial data, choosing a calculation method, and organizing cash movements into operating, investing, and financing sections. Here’s a straightforward breakdown of each step:

1. Choose the direct or indirect method

Decide how you want to handle the “operating activities” section. With the direct method, you list actual cash in (from customers) and cash out (to suppliers, payroll, rent, etc.). With the indirect method, you start with your profit and tweak it for things like non-cash expenses and invoices that are still unpaid.

2. Compute operating activities cash flow

Now, work out the cash from your day-to-day business. If you chose the direct method, add up all cash collected and subtract all cash paid for regular expenses. If you choose the indirect method, start with net income and adjust for items that affect cash, like customers who still owe you or bills you haven’t paid yet.

3. Compute investing activities cash flow

Next, look at big purchases and sales. Note any cash you spent on long-term things like equipment, vehicles, or software, and any cash you brought in from selling older assets.

4. Compute financing activities cash flow

Then, capture how money moved between you, lenders, and the business. Add cash from business loans or owner contributions, and subtract cash used for loan repayments or owner withdrawals.

5. Compute the ending cash balance

Add up net cash from operating, investing, and financing activities, then add that to the cash you had at the start of the period. That total is your ending cash balance.

6. Validate the cash flow statement

Finally, do a quick check: does your ending cash balance match what you see on your bank statement and balance sheet for the same date? If not, there’s probably a missing or misclassified cash movement to track down.

How to interpret positive cash flow

Positive cash flow means more cash is coming in than going out during the period. It increases the company’s available cash and can strengthen day-to-day stability, but the reason behind the positive number matters.

Positive operating cash flow usually signals a healthy core business. When a company consistently brings in more cash from customers than it spends on everyday expenses, it has room to cover bills, build savings, and reinvest.

- Example: A bakery that reliably collects cash from daily sales and keeps costs under control will show strong operating cash flow—even if profit margins fluctuate.

Positive investing cash flow typically means the business is selling assets. It may be strategic (selling old equipment to upgrade) or a sign that the company needs quick cash.

- Example: A landscaping company selling a retired mower will show positive investing cash flow, but repeated asset sales may hint at cash strain.

Positive financing cash flow reflects cash coming in from loans or owner contributions. It boosts liquidity now, but it also means future repayment obligations.

- Example: A startup taking out a $50,000 loan to hire staff will show positive financing cash flow even though the money isn’t earned through operations.

How to interpret negative cash flow

Negative cash flow means more cash left the business than came in during the period. It reduces available cash, but it’s not automatically a bad sign—it depends on why the cash went out.

Negative operating cash flow: This can mean the business isn’t generating enough cash to cover routine expenses. It might result from slow customer payments, rising costs, or weaker sales.

- Example: A consulting firm may show negative operating cash flow if most client invoices haven’t been paid yet, even if revenue looks strong.

Negative investing cash flow: This often indicates reinvestment—buying equipment, vehicles, or software. It lowers cash now but can support future growth.

- Example: A coffee shop renovating its space and buying new equipment will show negative investing cash flow during that period.

Negative financing cash flow: This usually means the business is paying down debt or the owner is taking distributions. Cash decreases, but it can be a sign of discipline rather than trouble.

- Example: A manufacturing business making a large loan repayment will show negative financing cash flow even when operations are solid.

Boost your cash flow with a business line of credit

When you need flexibility for situations like covering payroll during a slow month, buying inventory early, or bridging a gap from slow customer payments, having the right financing tool in place can make all the difference.

A business line of credit gives you that cushion. You can draw funds when you need them, repay, and draw again, without reapplying each time. It’s a practical way to strengthen cash flow and stay prepared for unexpected expenses or new opportunities.

Cash flow statement FAQs

How does a cash flow statement differ from a balance sheet?

A cash flow statement shows how much cash came in and went out during a period. A balance sheet is an overview of what your business owns (assets) and owes (liabilities) at a specific point in time. The cash flow statement focuses on movement, while the balance sheet focuses on position.

How do you build a cash flow statement from an income statement and a balance sheet?

Start with your income statement to get net income, then adjust it for noncash items (like depreciation) and changes in items from your balance sheet (such as accounts receivable, accounts payable, and inventory).

Then add cash activity from asset purchases/sales and loan activity from the balance sheet to complete the investing and financing sections. The final step is confirming that the beginning and ending cash numbers match your bank records.