Best Brex Alternatives & Competitors in 2026

Brex has become a go-to financial platform for venture-backed startups, combining corporate cards, AI-powered expense management, and business banking into a unified system. However, its focus on high-growth, incorporated companies comes with real limitations that leave many businesses looking elsewhere. Brex does not support sole proprietorships or unincorporated partnerships, requires businesses to meet stringent revenue or funding thresholds to qualify, and does not offer cash deposits or ATM access. With the Capital One $5.15 billion acquisition of Brex announced in early 2026, some finance leaders are also reconsidering their reliance on a platform now transitioning to a bank-led model.

For businesses that need broader accessibility, cash handling capabilities, or lending products, it is worth exploring what else the market offers. We will examine nine of the top Brex alternatives, including Bluevine, Mercury, Rho, and Ramp, to help you find a financial partner that matches your business structure, stage, and goals.

Highlights

- Brex excludes sole proprietorships and unincorporated businesses and typically requires venture funding or at least $400,000 in monthly revenue, putting it out of reach for many small businesses.

- Brex does not support cash deposits, ATM withdrawals, or debit cards tied to its checking account, which is a deal-breaker for businesses that handle physical cash.

- Bluevine fills the gaps Brex creates: it welcomes sole proprietorships and unincorporated businesses, lets customers deposit cash at over 90,000 locations,1 and pays up to 3.0% APY on checking balances2 without a venture-funding requirement.

- Bluevine also provides access to apply for a Bluevine Line of Credit3 and integrated invoicing tools. These are lending products that Brex does not offer.

- The best alternative depends on your specific priorities: whether that is earning interest on idle cash, managing international operations, or accessing working capital through a line of credit.

Why consider an alternative to Brex?

Brex can be an excellent platform for venture-backed startups and scaling tech companies that need sophisticated expense management, corporate cards with high limits, and international payment capabilities. Its AI-powered receipt matching, global card issuance in over 50 countries, and FDIC insurance up to $6 million are genuinely strong features for the right type of business.

That said, the specialized focus of Brex means it is not designed for, and actively excludes, a large segment of the business market. If your business does not fit its specific profile, you may encounter significant friction. A few Brex drawbacks to consider include:

- Restrictive eligibility requirements: Brex does not accept sole proprietorships, unincorporated partnerships, or general partnerships. It also typically requires venture backing or at least $400,000 in monthly revenue, making it inaccessible to many small and growing businesses.

- No cash deposits or ATM access: Brex is entirely digital with no connection to an ATM network and no facilities for depositing physical cash or checks. Businesses with any retail or cash-handling component will need a separate banking relationship.

- No debit cards: Brex issues only corporate credit/charge cards, not debit cards tied to its checking account. For businesses that prefer straightforward debit-based cash flow tracking, this creates an unnecessary layer of complexity.

- No lending products: Brex does not offer business lines of credit, term loans, or SBA loans. Companies that need access to working capital must establish separate lending relationships, adding friction to their financial stack.

Brex vs. competitors overview

1. Bluevine

Best for: Small businesses looking for an all-in-one digital banking platform

Brex vs. Bluevine: Bluevine is accessible to businesses of all structures and offers a high-APY checking account alongside lending products, while Brex restricts eligibility and lacks lending options.

Bluevine is an all-in-one banking platform that provides a complete financial solution for small businesses, including sole proprietorships, LLCs, and corporations. It combines a high-APY business checking account5 with lending products and integrated payment solutions like bill pay, invoicing, and payment links powered by Stripe.6 The Bluevine application process allows business owners to sign up for an account in just a few minutes, compared to the rigorous eligibility screening Brex requires.

Where Brex is built for venture-backed companies with complex expense management needs, Bluevine is designed for the broader small business market. Businesses can earn up to 3.0% APY on their checking balances,2 apply for a line of credit, subject to approval,3 and make cash deposits at over 90,000 locations through the Allpoint+ and Green Dot networks.1 Customers can also create up to 50 sub-accounts with an upgraded plan for budgeting purposes and manage all their financial operations from a single dashboard.

Additionally, Bluevine offers lending products that Brex simply does not. Eligible businesses can access a line of credit up to $250,000, subject to approval,3 and business term loans up to $500,000 through its partners, also subject to approval. Line of credit customers can access approved draws instantly in their Bluevine Business Checking account.7

Bluevine holds a 4.6 out of 5 rating (Excellent) on Trustpilot.8 Reviewers frequently praise the friendly and helpful customer service, along with the speed and efficiency of lending approval times.

Key features:

- High-yield business checking account with up to 3.0% APY2

- Up to 50 sub-accounts with an upgraded plan with automatic transfer rules

- Built-in invoicing and accounts payable tools

- Multiple checking plans, all with FDIC insurance up to $3 million through Coastal Community Bank, Member FDIC and partner banks4

- Access to apply for a Bluevine Line of Credit3 and business term loans, subject to approval

Pricing:

- Standard plan: Free, with 1.3% APY on balances up to $250,000 (activity requirements apply)

- Plus plan: $30/month, or $0/month if you meet fee waiver requirements9

- Premier plan: $95/month, or $0/month if you meet fee waiver requirements10

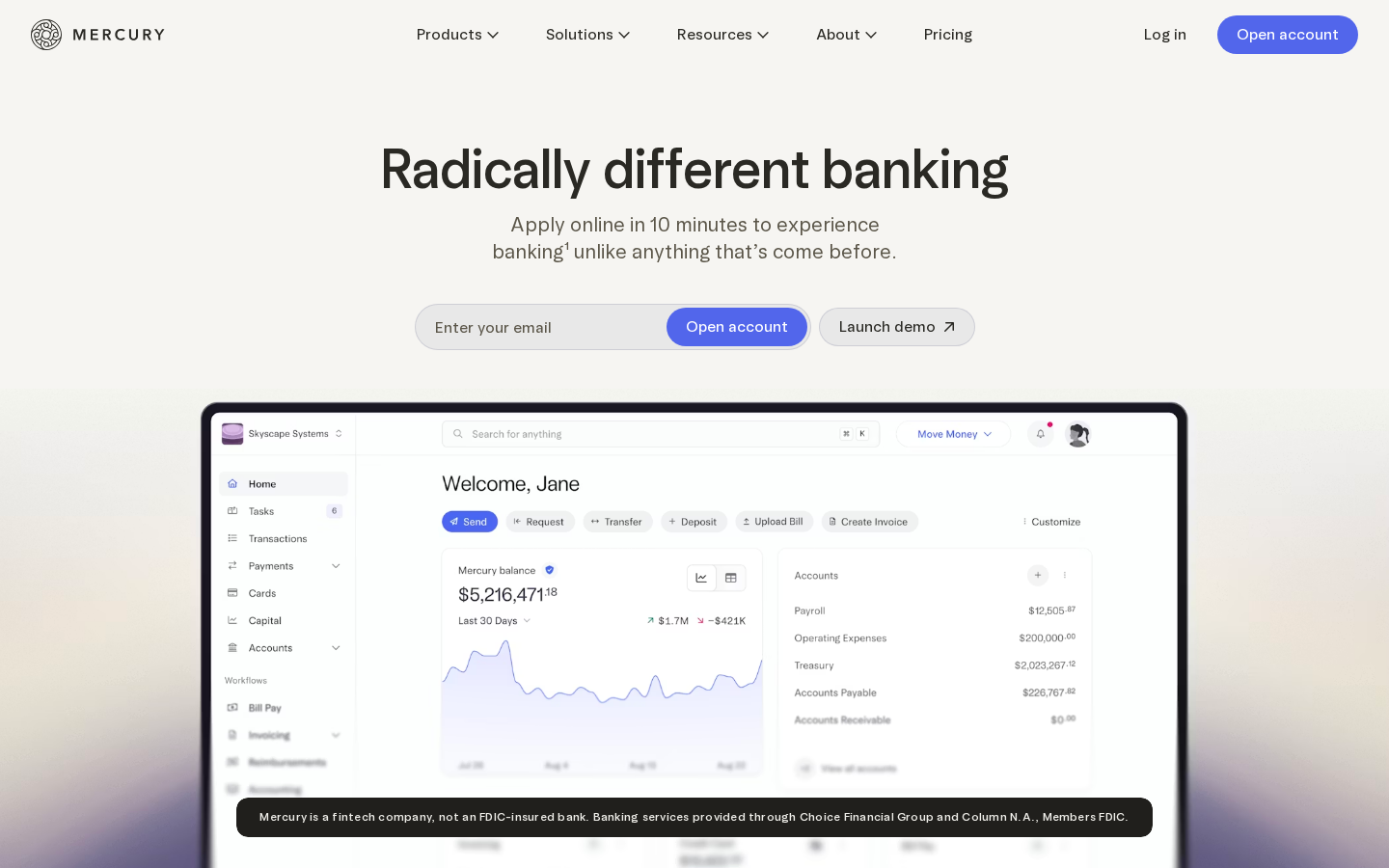

2. Mercury

Best for: Tech startups needing developer-friendly banking tools

Brex vs. Mercury: Mercury opens its doors to a wider range of startups with lower qualification barriers and no minimum revenue requirements, while Brex demands venture funding or significant monthly revenue to get started.

Mercury has become one of the most popular banking platforms for tech startups, and for good reason. Its sleek digital interface, read-write API access, and deep integrations with tools like QuickBooks and Xero make it a natural fit for digitally native companies. Mercury offers free domestic and international USD wires, a meaningful cost savings compared to traditional banks, and FDIC insurance up to $5 million through its partner banks.

For companies with substantial cash reserves ($250,000+), Mercury Treasury provides access to high-yield money market funds. The platform also supports venture debt for qualifying startups and recently launched Mercury Personal, a banking product for founders. That said, Mercury shares some of the Brex limitations: it does not support sole proprietorships, does not accept cash deposits, and its standard savings account earns no interest. The paid plans (starting at $35/month) are required for advanced accounting integrations.

Users on Trustpilot praise the intuitive Mercury interface and free wire transfers, though some report delays with check deposits and occasional account closures.

Key features:

- FDIC insurance up to $5 million via partner banks

- Free domestic and international USD wire transfers

- Read-write API access for custom automations and dashboards

Pricing:

- Free core banking with no monthly fees

- Mercury Plus: $35/month; Mercury Pro: $350/month

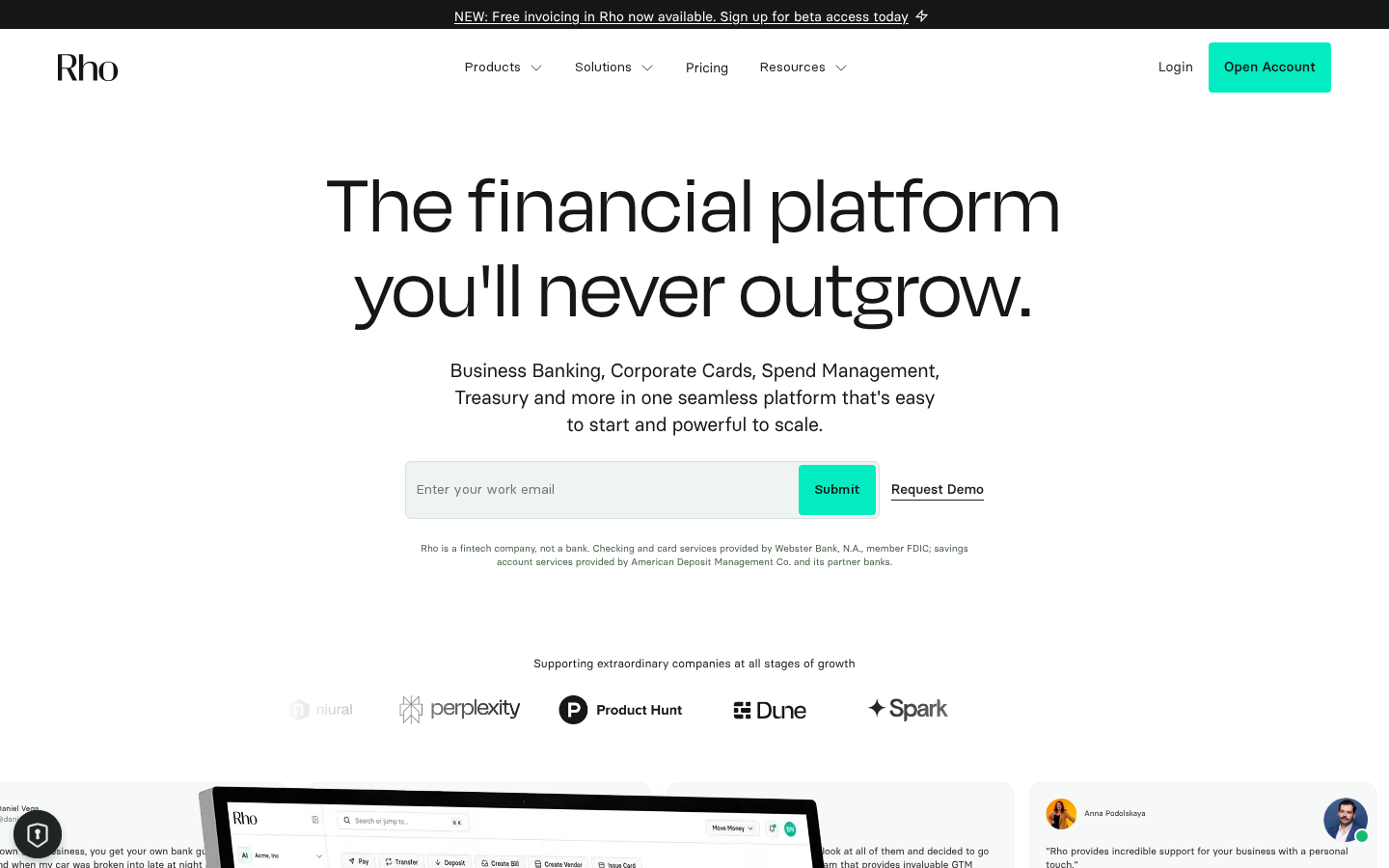

3. Rho

Best for: High-growth businesses that need integrated banking with dedicated support

Brex vs. Rho: Rho provides every customer, regardless of size, with a dedicated banking specialist and 24/7 support, while Brex reserves its more personalized support tiers for Premium and Enterprise subscribers.

Rho positions itself as a unified financial platform that combines business checking, corporate cards, expense management, and accounts payable automation, all with no subscription or per-user fees. That pricing model stands in sharp contrast to the Brex $12/user/month Premium plan, making Rho a particularly cost-effective choice for growing teams.

The platform’s corporate Mastercard earns up to 1.25% cashback (or 2% with the Rho Platinum Card for combined banking and card customers) with no annual fees. Rho also offers fee-free domestic payments, including same-day ACH and wire transfers, and savings accounts with an impressive $75 million in FDIC coverage. Like Brex, however, Rho does not support sole proprietorships or cash deposits. Its services require incorporated U.S. businesses.

Users on Trustpilot like the attentive Rho customer service and smooth onboarding, though some complain of occasional communication issues and shifting rates.

Key features:

- Dedicated specialist and 24/7 support for all customers

- Fee-free domestic same-day ACH and wire transfers

- Corporate cards with up to 2% cashback (Platinum tier)

Pricing:

- Free platform with no subscription or per-user costs

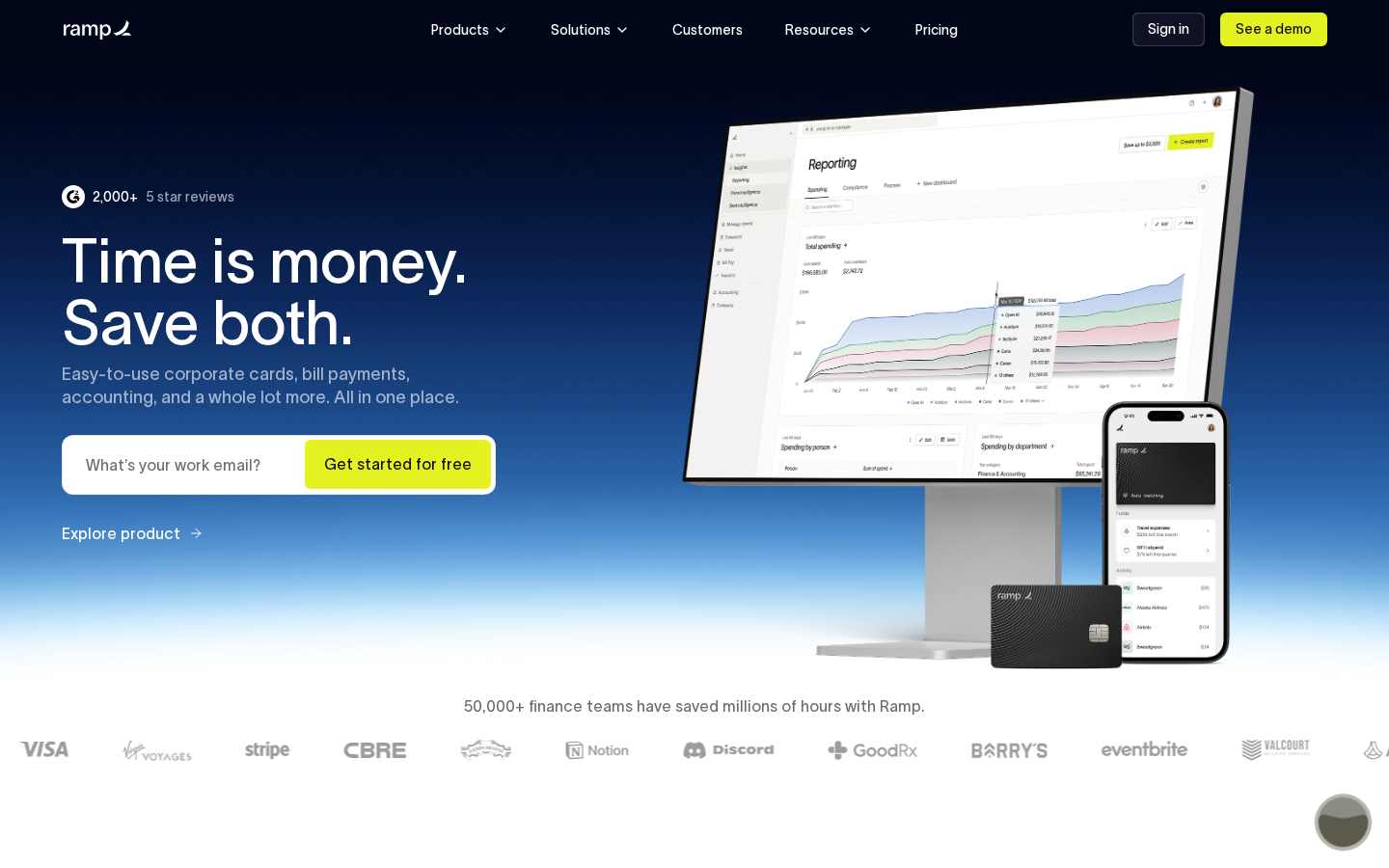

4. Ramp

Best for: Companies focused on spend management and cost reduction

Brex vs. Ramp: Ramp offers a straightforward flat 1.5% cashback on all purchases with no points system, whereas Brex uses a tiered points-based rewards structure that recently devalued to as low as 0.6 cents per point for cash redemptions.

Ramp was built with one core mission: help companies spend less. Its AI-powered expense management system automatically collects, matches, and categorizes receipts while enforcing spending policies, eliminating the need for manual expense reports. The flat 1.5% cashback on Ramp corporate cards is simple and transparent, a contrast to the Brex category-based rewards system.

Beyond expense automation, Ramp offers a full procure-to-pay suite for managing vendor invoices, purchase orders, and multi-level approval workflows. The free core platform includes corporate cards, expense management, and bill pay. However, Ramp is primarily a spend management platform, not a full-service banking solution, so businesses may need a separate bank account for their core banking needs.

Users on Trustpilot praise the time-saving Ramp automation features, but some criticize the company for inconsistent customer service.

Key features:

- AI-powered software to eliminate manual expense reports

- Corporate cards with flat 1.5% cashback and granular spending controls

- Full procure-to-pay suite for managing vendors and bills

Pricing:

- Core Ramp platform: Free

- Ramp Plus: $15/user/month

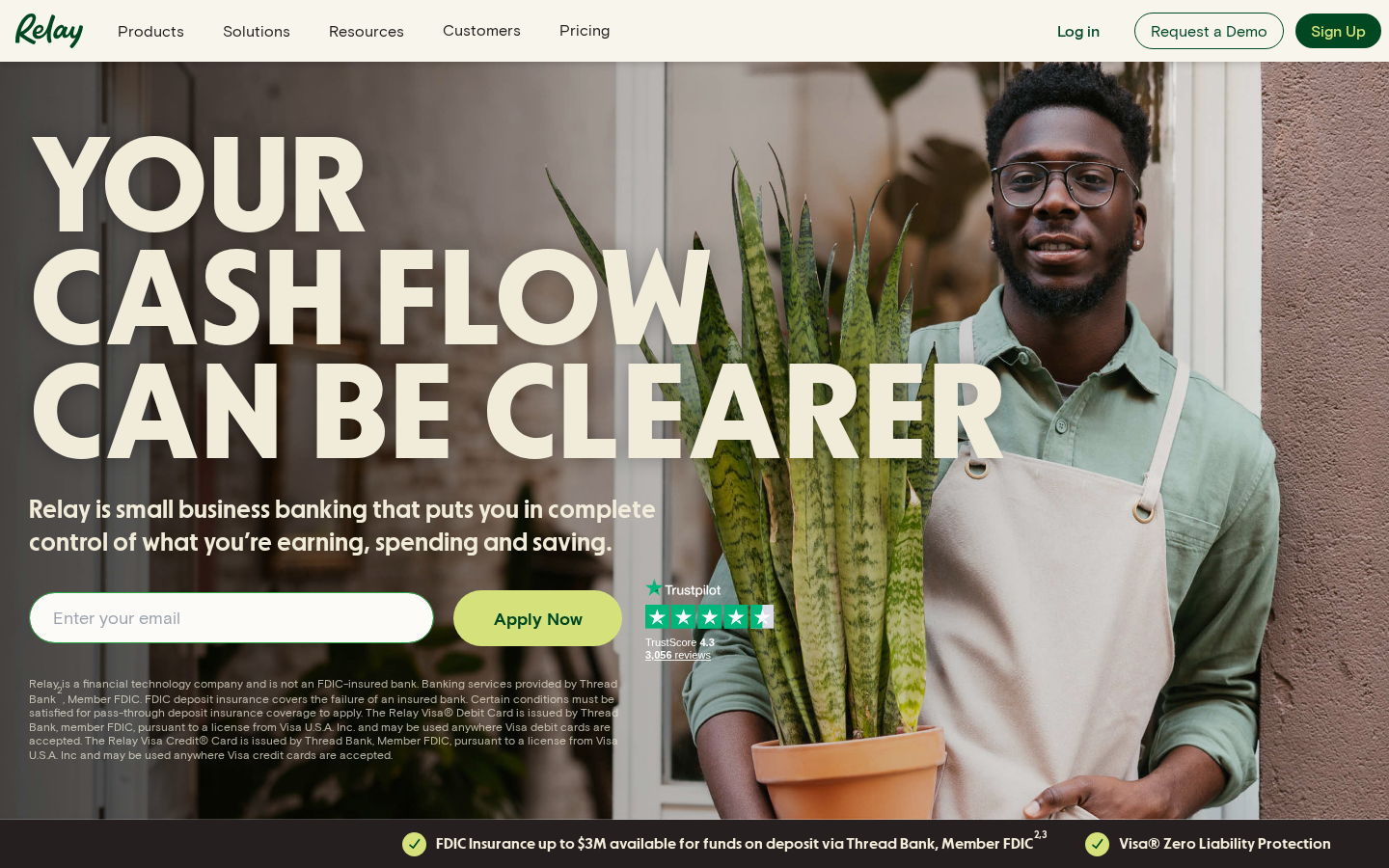

5. Relay

Best for: Businesses that need multiple checking accounts and cash deposit access

Brex vs. Relay: Relay offers up to 20 fee-free checking accounts and granular, multi-account cash flow organization. These are practical banking capabilities that Brex does not provide.

Relay is designed for small and medium-sized businesses that want granular cash flow management. The platform allows users to create up to 20 fee-free checking accounts on its free Starter plan, making it popular among businesses that follow budgeting methodologies like Profit First. Relay also supports team collaboration with up to 50 physical and virtual Visa debit cards with customizable spending limits. Paid Grow and Scale plans add advanced accounts payable automation, higher savings APY, and reduced wire transfer fees.

The platform offers a competitive, tiered APY on its business savings account. However, this APY does not extend to its checking accounts, a limitation for businesses that want their working capital to earn interest. Relay also lacks lending products, which may be a factor for businesses seeking a more comprehensive financial platform.

Users on Trustpilot find the Relay setup process straightforward and like the multi-account structure, but some have complained of frozen accounts and communication gaps.

Key features:

- Create up to 20 individual fee-free checking accounts

- Issue up to 50 virtual and physical debit cards with spending controls

- Low-cost wire transfers ($8 domestic on Starter; reduced fees on Grow and Scale plans)

Pricing:

- Starter plan: Free

- Grow plan: $30/month

- Scale plan: $90/month

6. Novo

Best for: Freelancers, solopreneurs, and small business owners

Brex vs. Novo: Novo welcomes the businesses that Brex turns away (sole proprietors, freelancers, and independent contractors) by offering a free checking account with unlimited invoicing and no minimum balance requirements.

Novo is a mobile-first banking platform specifically designed for the smallest segment of business owners. While Brex caters to venture-backed companies, Novo focuses on simplicity and accessibility. Business owners can create, send, and manage professional invoices directly from the app, with options to accept payment via ACH or through Stripe and Square integrations.

The Novo Reserves feature allows users to create up to 20 Reserve categories for setting aside funds for taxes, profit, or other specific goals. The platform also provides flexible ATM access, refunding up to $7 per month in third-party ATM fees. While Novo is a strong entry-level solution, it does not offer interest on checking balances, lending products, or sub-account functionality beyond Reserves.

Users on Trustpilot like the clean Novo interface, but some have voiced frustration with customer support response times and account closure policies.

Key features:

- Reserves feature for setting aside funds for taxes or other goals

- Refunds up to $7 per month in third-party ATM fees

- Unlimited built-in invoicing directly from the app

Pricing:

- Free business checking with no monthly fees

7. Airbase

Best for: Mid-market companies with complex procurement needs

Brex vs. Airbase: Airbase provides enterprise-grade AP automation with purchase order management and three-way matching capabilities that go beyond the Brex bill pay features.

Airbase is not a banking platform in the traditional sense. Rather, it is a comprehensive procure-to-pay spend management system. The platform includes AP automation designed to handle complex scenarios like two-way and three-way matching and multi-subsidiary accounting. Deep integrations from Airbase with enterprise ERP systems like NetSuite and Sage Intacct make it a strong fit for mid-market companies that have outgrown simpler tools.

The trade-off is that Airbase requires quote-based pricing, which may put it out of reach for smaller businesses, and it does not include core banking services like checking accounts.

Users on G2 enjoy the streamlined Airbase expense management, but dislike its receipt handling and report upload experience.

Key features:

- Advanced AP automation with purchase order and three-way matching

- Deep integrations with enterprise ERP systems like NetSuite

- Guided procurement with multi-stakeholder approval workflows

Pricing:

- Quote-based pricing

8. NorthOne

Best for: Main Street small businesses and local shops

Brex vs. NorthOne: NorthOne is purpose-built for traditional small businesses that need straightforward banking with cash deposit access, a segment that the Brex digital-only, startup-focused model does not serve.

NorthOne is built for a different kind of business than Brex. Where Brex serves tech companies operating at scale, NorthOne is designed for the local business owner: the contractor, the restaurant, the retail shop. The platform provides a simple business checking account with sub-accounts, built-in invoicing, and cash deposit capabilities through the Green Dot retail network.

The NorthOne interface is clean and focused on the essentials. However, its feature set is relatively basic compared to other fintech platforms, and it lacks lending products, high-yield interest options, and advanced expense management tools.

Key features:

- Sub-accounts for organizing funds by purpose (taxes, payroll, expenses)

- Cash deposits via the Green Dot retail network

- Built-in invoicing and automatic bookkeeping features

Pricing:

- Free basic plan; Plus plan: $10/month

9. Arc

Best for: VC-backed startups focused on maximizing treasury yield

Brex vs. Arc: The core Arc differentiator is its treasury management product, which allows startups to earn competitive yields on idle cash through diversified, institutional-grade investment options.

Arc is a financial platform built specifically for venture-backed startups that want to maximize the return on their idle cash. The platform provides business banking alongside a treasury product designed to help companies extend their runway. Arc also offers tools for managing SAFEs and fundraising workflows, features that are particularly useful for early-stage startups navigating their first rounds of funding.

The narrow Arc focus on the startup ecosystem means it lacks the breadth of features (such as lending products, invoicing, or cash deposit access) that broader platforms provide. Arc currently has limited reviews on major platforms.

Key features:

- High-yield treasury management on idle cash

- SAFE and fundraising workflow tools

- Startup-specific banking integrations and features

Pricing:

- Free core banking; treasury management fees vary

How to find the best banking platform for your growing business

Choosing the best banking platform requires a thorough review of how it aligns with your business’s operational model, cash management strategy, and growth trajectory.

- Accessibility and convenience: Consider your day-to-day banking needs, from the quality of the mobile app to whether you need cash deposit capabilities. Platforms like Bluevine (with 90,000+ deposit locations)1 have a clear advantage over digital-only options like Brex.

- Financial needs: Match the platform’s tools to your cash flow requirements. Do you need fee-free wire transfers, integrated invoicing, or corporate cards with spend controls?

- Interest rates and loan options: Compare the APY offered on checking and savings accounts. Also review available financing. Bluevine, for example, offers both a line of credit and term loans alongside its checking account, subject to approval.3

- Pricing and fees: Look beyond the monthly fee and analyze the entire cost structure, including per-user fees, wire transfer charges, and foreign exchange markups.

- Reputation and stability: Evaluate the platform’s track record and look for enhanced FDIC insurance beyond the standard $250,000 limit. Bluevine offers FDIC insurance up to $3 million.4

Business growth starts with the right financial foundation

The right banking platform should fit your business as it is today and scale with you as you grow. For many small and growing businesses, the restrictive Brex eligibility requirements, lack of lending products, and absence of cash deposit capabilities create real gaps.

A Bluevine Business Checking account addresses these gaps directly. It offers a high APY on checking balances,5 supports cash deposits at over 90,000 locations,1 and serves businesses of all structures, including the sole proprietorships and small LLCs that Brex turns away. Combined with lending products (subject to approval),3 integrated invoicing, and accounts payable tools, Bluevine provides the all-in-one financial platform that growing businesses need.

Sign up for a Bluevine Business Checking account and see what it can do for your business.

FAQs

answer

Disclaimers

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

‡ The national average and comparison are based on interest rates paid by U.S. depository institutions as calculated by the FDIC.

◊ Applications are subject to credit approval. Rates and terms may vary based on your creditworthiness and are subject to change. Eligibility for the maximum funding amount is available only to applicants with the strongest credit profiles. Offerings and eligibility requirements vary by partner.

1. A $4.95 per transaction fee is applicable when depositing funds at Green Dot® locations. A fee of $1.00 plus 0.5% of your total deposit amount applies when depositing funds at Allpoint+ ATMs.

2. Bluevine Premier customers will earn 3.0% annual percentage yield ("APY") on total Bluevine Business Checking balances. Any interest accrued and payable for an account or sub-account will be paid to your main account. Enrollment in Bluevine Premier is not required to receive increased FDIC insurance coverage. Customers automatically receive increased FDIC coverage unless they have opted out of the Bluevine Business Checking Account Agreement Sweep Program.

3. Applications are subject to credit approval. Rates, credit lines, and terms may vary based on your creditworthiness and are subject to change. Eligibility for the lowest rates is available only to applicants with the strongest credit profiles. Factors include FICO score, time in business, monthly revenue, and payment history. Additional fees apply. Bluevine Flex Line of Credit is issued by Celtic Bank, a Utah-chartered Industrial Bank, Member FDIC.

4. Bluevine accounts are FDIC insured up to $3,000,000 per depositor through Coastal Community Bank, Member FDIC and our program banks. $3,000,000 in FDIC insurance is offered by multiplying the standard $250,000 FDIC coverage across multiple banks.

5. Premier and Plus plan customers automatically earn annual percentage yield ("APY") on their available balances. Standard plan customers will earn interest on their available balances if they meet an eligibility requirement as detailed in the Terms of Interest Accrual which is incorporated as a part of the Bluevine Business Checking Account Agreement. Bluevine Premier is subject to a $95 monthly fee. Bluevine Plus is subject to a $30 monthly fee.

6. Payment processing services are provided by Stripe, Inc., N.A. Bluevine Inc. Payment processing services are available to most businesses, subject to eligibility determined by Bluevine.

7. Draw requests are subject to review and approval. Bluevine Line of Credit customers can access approved draws instantly only with their Bluevine Business Checking account. Approved draws being deposited to an external bank account will be available in as quickly as a few hours if you choose our bank wire option ($15). Or, choose our fee-free ACH transfer option which typically gets funds deposited the next business day, although it may take up to three. Bluevine Flex Line of Credit is issued by Celtic Bank, a Utah-chartered Industrial Bank, Member FDIC.

8. Ratings as of March 2026.

9. Bluevine Plus is subject to a $30 monthly fee. Avoid the fee by doing the following each billing period: 1) maintain an average daily balance of at least $20,000 in your Bluevine Business Checking account and/or sub-account(s) and 2) spend at least $2,000 with your Bluevine Business Debit Mastercard® or Bluevine Business Cashback Mastercard®.

10. Bluevine Premier is subject to a $95 monthly fee. Avoid the fee by doing the following each billing period: 1) maintain an average daily balance of at least $100,000 in your Bluevine Business Checking account and/or sub-account(s) and 2) spend at least $5,000 with your Bluevine Business Debit Mastercard® or Bluevine Business Cashback Mastercard®.

Bluevine is a financial technology company, not a bank. Banking Services provided by Coastal Community Bank, Member FDIC. FDIC insurance only covers the failure of an FDIC-insured bank. FDIC insurance is available through pass-through insurance at Coastal Community Bank, Member FDIC, if certain conditions have been met. Bluevine accounts are FDIC insured up to $3,000,000 per depositor through Coastal Community Bank, Member FDIC and our program banks. The Bluevine Business Debit Mastercard® and Bluevine Business Cashback Mastercard® are issued by Coastal Community Bank, Member FDIC pursuant to a license from Mastercard International Incorporated and may be used everywhere Mastercard is accepted. Mastercard is a registered trademark and the circles design is a trademark of Mastercard International Incorporated.

Mastercard, Mastercard Easy Savings, Mastercard Airport Concierge, Priceless Surprises and the circles design are registered trademarks and Mastercard ID Theft Protection is a trademark of Mastercard International Incorporated.

Application is subject to approval. No monthly or maintenance fees. Card Replacement Fees and Wire Transfer Fees may apply.

Banking Services for payments made via ACH or wire from the Bluevine Business Checking Account are provided by Coastal Community Bank, Member FDIC. Money transmission services for International Payments are provided by a third party and are also subject to their applicable terms and conditions.

The Bluevine Line of Credit is issued by Celtic Bank and is serviced by Bluevine. Applications are subject to credit approval. Rates, credit lines, and terms may vary based on your creditworthiness and are subject to change. Additional fees apply. Other commercial credit products are offered by a variety of Bluevine’s third party partners. Bluevine is not involved in the issuance or servicing of these products. Offerings and eligibility requirements vary by partner.

Certain financing may be made or arranged pursuant to California Financing Law-License No. 6054789.

Payment processing services are provided by Stripe, Inc., N.A. Bluevine Inc. Payment processing services are available to most businesses, subject to eligibility determined by Bluevine.

Tap to Pay is only available on supported devices and may require upgrading to the latest version of the Bluevine app and your phone’s operating system. Some Android devices may not be compatible. Android is a trademark of Google LLC. Tap to Pay on iPhone requires a supported payment app. Some contactless cards may not be accepted by your payment app. Transaction limits may apply. The Contactless Symbol is a trademark owned by and used with permission of EMVCo, LLC. Tap to Pay on iPhone is not available in all markets. For Tap to Pay on iPhone countries and regions, see here.

All other product names, logos, brands, trademarks, and registered trademarks are property of their respective owners. All company, product, and service names used in this website are for identification purposes only. Use of these names, trademarks, and brands does not imply endorsement.

® 2026 Bluevine Inc. All Rights Reserved. “Bluevine” and the Bluevine logo are registered trademarks of Bluevine Inc.