The 8 Bill.com Alternatives to look at in 2026

Bill.com, now known as BILL, has long been one of the most recognized names in accounts payable and receivable automation. The platform helped pioneer cloud-based bill pay for small businesses and continues to serve a large customer base. But as the financial software market has matured, a growing number of businesses are finding that BILL's per-user pricing, per-transaction fees, and lack of a native business bank account leave gaps that other platforms fill more effectively. If you are evaluating your options, this guide covers eight alternatives, including Bluevine, Melio, Ramp, Tipalti, Stampli, Brex, QuickBooks Online, and AvidXchange, so you can find the platform that best fits how your business manages money.

Highlights

- BILL's per-user pricing starts at $45/user/month for its AP and AR plans, and most payment methods carry additional per-transaction fees. For teams with more than a few users, costs can add up quickly.

- BILL is a payment automation tool, not a bank. It connects to your existing checking account but does not offer interest on deposits, FDIC insurance on its own, or built-in lending products. Bluevine combines checking with up to 3.0% APY1, FDIC coverage up to $3 million through Coastal Community Bank, Member FDIC and partner banks2, and access to apply for a line of credit3 in one platform.

- Unlike BILL, Bluevine offers cash deposits at over 90,000 locations through the Allpoint+ and Green Dot® networks4, making it a practical choice for businesses that handle physical cash.

- The right alternative depends on your payment volume, team size, whether you operate globally, and whether a banking relationship matters alongside your AP/AR workflow.

- BILL holds a 3.1 out of 5 rating on Trustpilot. Reviewers consistently flag slow customer support response times and unexpected payment holds as their biggest frustrations.

Why consider an alternative to Bill.com?

BILL was built to help small businesses digitize paper-based AP workflows, and it does that reasonably well. Businesses that already use QuickBooks or Xero and process a high volume of vendor bills will find the accounting sync useful, and the platform's approval workflow features are solid for teams with multiple approvers.

That said, BILL is not the right fit for every business. The platform's pricing model, feature gaps, and lack of native banking lead many growing companies to look elsewhere. Here are the most common reasons businesses seek an alternative.

- Per-user fees scale quickly: BILL charges $45 to $89 per user per month for its AP/AR plans, plus additional fees for each ACH transfer, check, or instant payment. A small finance team of three to five users can easily spend several hundred dollars per month on subscription costs alone before accounting for transaction fees.

- No native business banking: BILL is a payment software layer that sits on top of your existing bank account. It does not offer FDIC-insured deposits, interest on checking balances, a debit card, or cash deposit access. For businesses that want a single platform handling both their banking and their AP/AR workflows, BILL requires pairing with a separate banking product.

- Limited lending access: BILL does not offer business loans or lines of credit. If access to working capital is important to your business, you will need a separate relationship with a lender or bank.

- Mixed customer support reviews: BILL holds a 3.1 out of 5 rating on Trustpilot, with frequent complaints about payment holds, difficulty reaching support agents, and unresolved issues for small businesses. Businesses that need reliable, responsive support when payments are time-sensitive may find this a meaningful trade-off.

Bill.com vs. competitors overview

1. Bluevine

Best for: Small and medium-sized businesses that want a fully integrated banking and financial operations platform

Bill.com vs. Bluevine: Unlike BILL, Bluevine provides a full-featured business checking account with high-yield interest, built-in invoicing, and access to apply for a line of credit3, eliminating the need to manage a separate bank alongside your AP/AR software.

Bluevine is an all-in-one business banking platform designed for small and medium-sized businesses across all structures, including sole proprietors, LLCs, S-corps, and C-corps. Where BILL functions as a payment automation layer that connects to an external bank, Bluevine is the bank. Eligible businesses earn up to 3.0% APY1 on their checking balance, get FDIC insurance up to $3 million through Coastal Community Bank, Member FDIC and partner banks2, and manage invoices and bill pay from the same account dashboard.

A key differentiator for businesses with cash-heavy operations: Bluevine supports cash deposits at over 90,000 locations through the Allpoint+ and Green Dot® networks4. Stripe-powered payment links5 let you collect customer payments digitally without a separate merchant account. Up to 50 sub-accounts with an upgraded plan keep different cash flows organized without the complexity of multiple bank accounts.

Eligible businesses can also access a Bluevine Line of Credit up to $250,0003 and term loans up to $500,000 through partners for approved customers, giving Bluevine a financing dimension that BILL simply does not offer. Instant draws are available for approved Bluevine Line of Credit customers with a Bluevine Business Checking account6.

Bluevine holds a 4.6 out of 5 rating (Excellent) on Trustpilot. Reviewers frequently praise the straightforward account setup, responsive customer support, and the speed of lending approval. Some users note that the mobile app can feel limited compared to desktop, though Bluevine has continued to expand its app functionality.

Key features:

- Checking earns up to 3.0% APY (Premier plan)1 on balances up to $3 million

- FDIC insured up to $3 million through Coastal Community Bank, Member FDIC and partner banks2

- Cash deposits at 90,000+ Allpoint+ and Green Dot® locations4

- Integrated invoicing with Stripe-powered payment links5 and bill pay

- Access to apply for a line of credit up to $250,0003 and term loans through partners for approved customers

Pricing:

- Standard: Free. Earns 1.3% APY on balances up to $250,000 (if monthly activity requirements met)

- Plus: $30/month, or $0/month if you meet fee waiver requirements7

- Premier: $95/month, or $0/month if you meet fee waiver requirements8. Earns 3.0% APY on balances up to $3 million

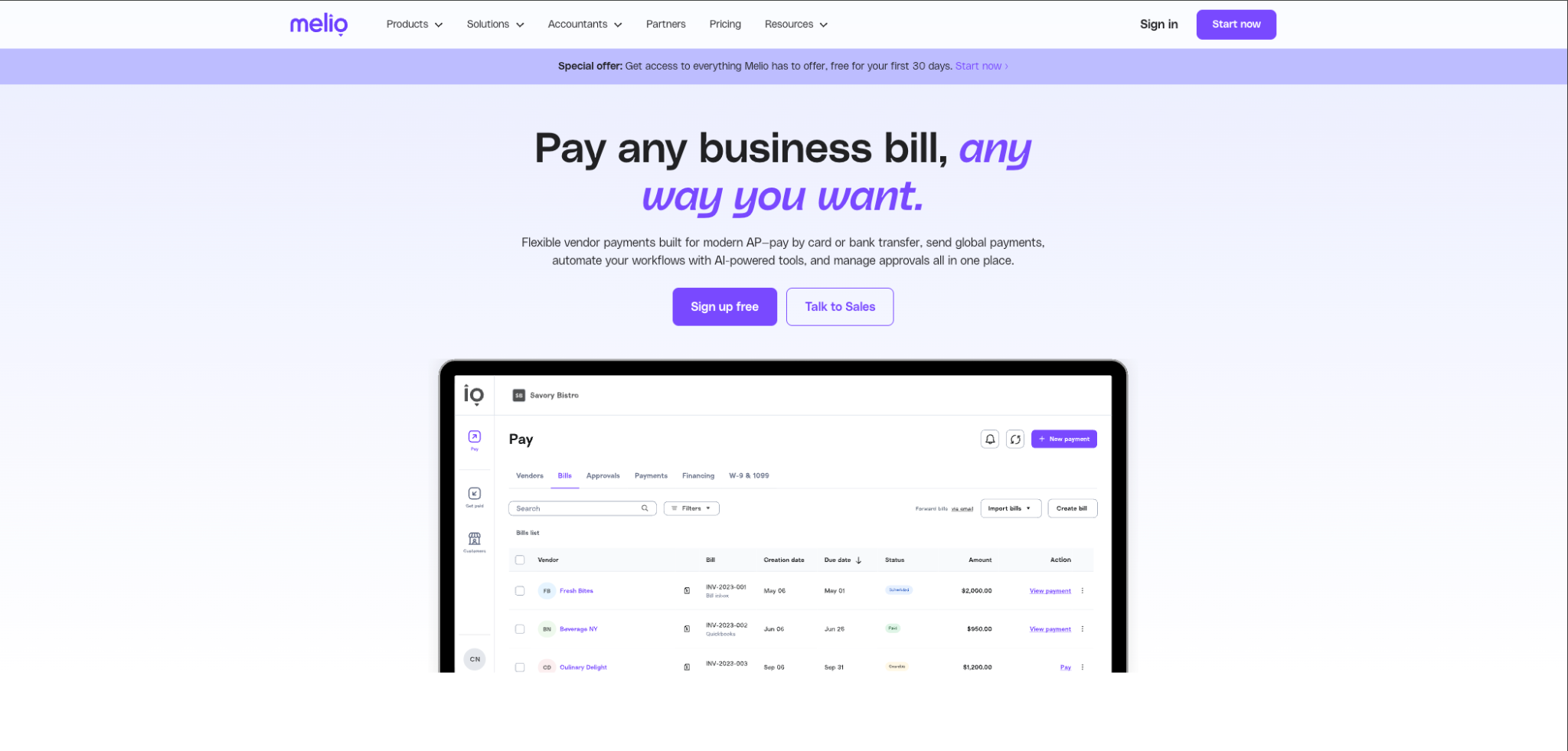

2. Melio

Best for: Small businesses seeking an affordable, straightforward bill-pay solution with free ACH and QuickBooks integration

Bill.com vs. Melio: Melio's free Go plan and affordable paid tiers offer a meaningfully lower total cost than BILL for small teams, and unlike BILL, Melio does not charge per-user subscription fees on its base plans.

Melio is a payment platform built for small businesses that want to pay vendors quickly and without complexity. Recently acquired by Xero for $2.5 billion, Melio offers a free entry plan that covers ACH payments and basic invoicing, making it one of the most accessible options for businesses with modest payment volumes. For larger teams, paid plans ranging from $25 to $80 per month unlock batch payments, approval workflows, and deeper QuickBooks and Xero integration.

One of Melio's most practical features is the ability to pay vendors by credit card even when those vendors only accept checks. Melio handles the conversion, letting businesses extend payment float or earn card rewards on vendor payments. The platform also supports W-9 collection and 1099 automation on paid plans, a useful addition for businesses working with contractors.

Where Melio falls short: it is a payments tool, not a bank, so it shares BILL's core limitation of requiring a separate banking relationship. AR functionality is basic compared to dedicated invoicing platforms. Reviewers on G2 frequently cite ACH processing delays and limited customer support responsiveness on lower-tier plans as frustrations.

Melio earns a 4.2 out of 5 on Capterra. Users praise its ease of use and the cost savings from free ACH payments; the most common criticisms are around payment delays and limited phone support on entry-level plans.

Key features:

- Free ACH payments on paid tiers (Go plan: 5 free/month)

- Pay vendors by credit card even where cards are not accepted (2.9% fee)

- Two-way QuickBooks Online/Xero sync and W-9/1099 automation

Pricing:

- Go (Free): 5 free ACH/month, basic features

- Core: $25/month (20 free ACH, batch payments, QuickBooks sync)

- Boost: $55/month (50 free ACH, QuickBooks Desktop, advanced approvals)

- Unlimited: $80/month (unlimited ACH and user seats)

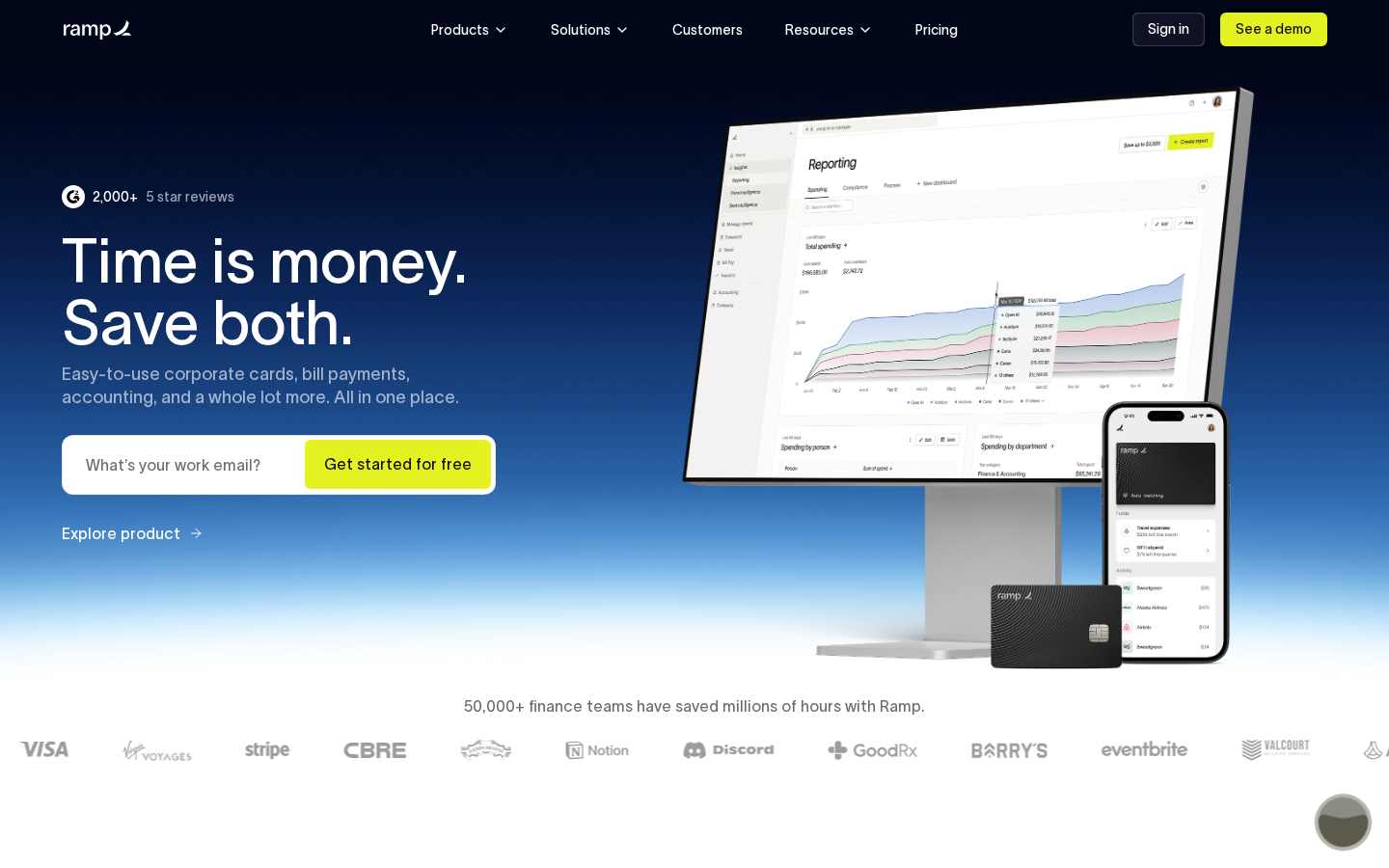

3. Ramp

Best for: Cost-conscious small and mid-size businesses that want AI-powered AP automation combined with spend management at no software cost

Bill.com vs. Ramp: Ramp's core AP and spend management features are free, compared to BILL's $45+ per-user monthly fee, and Ramp bundles corporate card management alongside its bill pay capability.

Ramp is a spend management and AP automation platform built around a no-software-fee model. The free tier includes AI-powered bill pay with high-accuracy OCR invoice capture, unlimited corporate cards, approval workflows, and basic spend controls. Ramp generates revenue through its corporate card program rather than software subscriptions, making it an attractive option for businesses looking to consolidate their payment stack without adding monthly SaaS costs.

The platform has invested heavily in AI automation: its bill pay product handles invoice ingestion, data extraction, approval routing, and payment execution with minimal manual intervention. Ramp also includes price intelligence features that surface savings opportunities across vendor contracts, a capability BILL does not offer.

The trade-off is that Ramp's card-centric model works best for businesses that adopt its corporate card program. Some advanced features, such as multi-entity support, foreign currency payments, and deeper ERP integrations, require Ramp Plus at $15 per user per month. Ramp also does not provide business banking, interest on deposits, or lending products.

Ramp earns a 4.8 out of 5 on G2 across thousands of reviews. Users consistently highlight the speed of the onboarding process, the quality of the expense management features, and the platform's savings recommendations as standout qualities.

Key features:

- Free AI-powered bill pay with OCR invoice capture and approval workflows

- Unlimited corporate cards with real-time spend controls and budgeting

- Vendor price intelligence and savings recommendations

Pricing:

- Free tier: Core bill pay, unlimited cards, basic approval workflows

- Ramp Plus: $15/user/month (multi-entity, foreign currency, advanced ERP integrations)

- Enterprise: Custom pricing

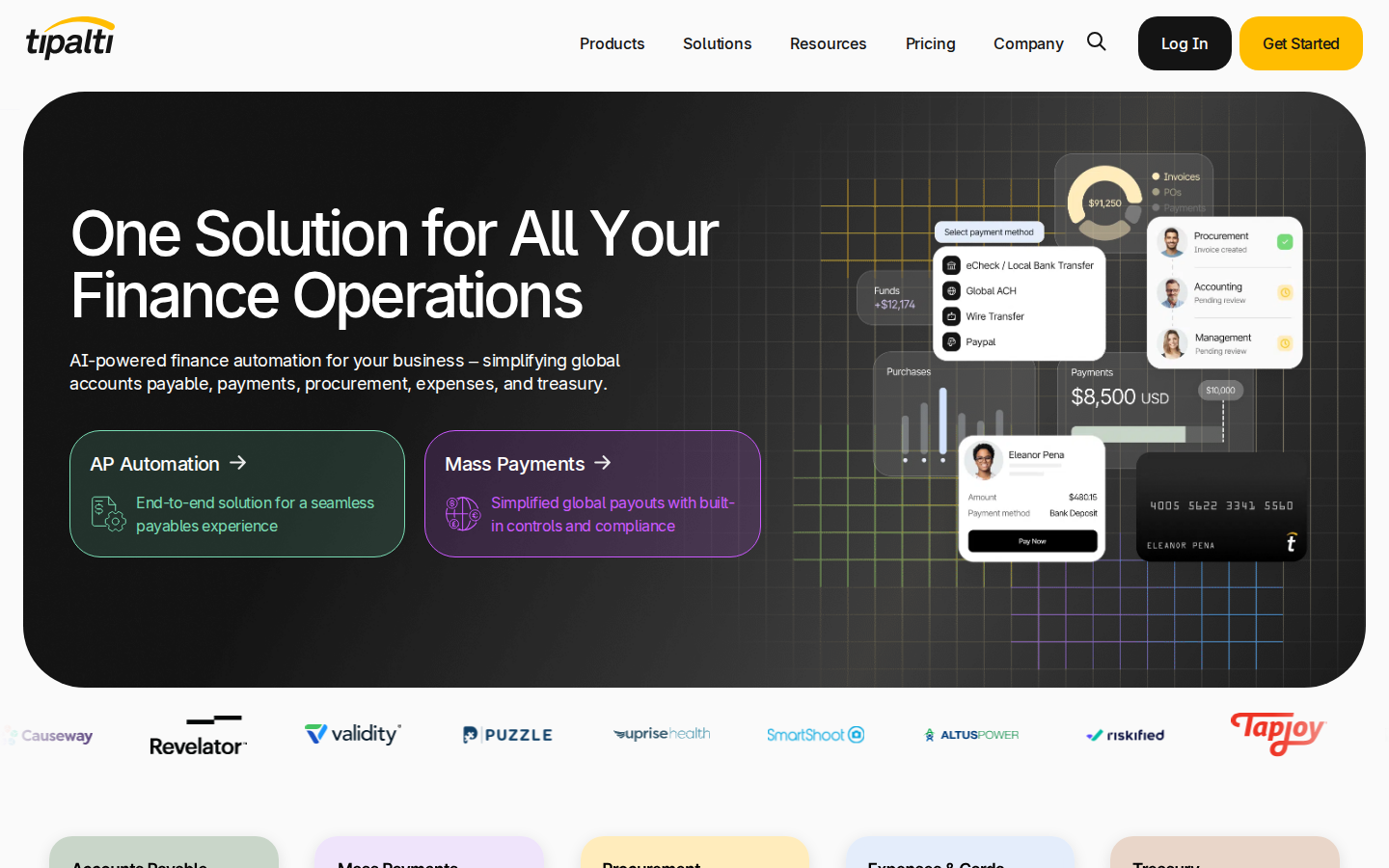

4. Tipalti

Best for: Mid-market companies managing high volumes of global vendor payments with complex tax and compliance requirements

Bill.com vs. Tipalti: Tipalti's global payment infrastructure supports 196 countries and 120+ currencies with built-in tax compliance, while BILL's international payment capabilities are significantly more limited.

Tipalti is purpose-built for companies that pay large numbers of suppliers globally. Its supplier onboarding portal collects banking details, tax forms (W-9, W-8BEN, VAT IDs), and payment preferences directly from vendors, reducing the administrative burden on AP teams. The platform's KPMG-approved tax and VAT compliance engine validates tax IDs and generates 1099 and 1042-S reports at year-end.

For companies processing millions in monthly vendor payments across multiple currencies and entities, Tipalti's automation reduces manual workload significantly. Customers like GoDaddy and Roku use it for mass payouts at scale. The platform integrates with NetSuite, QuickBooks, Xero, and Sage Intacct for reconciliation.

Tipalti is not the right fit for smaller businesses or those with straightforward domestic AP workflows. Starting at $99 per month for the platform fee, with custom pricing for volume and advanced modules, it is priced for the mid-market. The interface can be slow and complex for new users, and Tipalti does not offer banking, interest on deposits, or lending.

Tipalti earns a 3.3 out of 5 on Trustpilot, with reviews divided between businesses that praise its automation and global capabilities and those who cite high transaction fees and occasional payment errors. On G2, where reviews skew toward enterprise users, the platform rates significantly higher.

Key features:

- Global payments to 196 countries in 120+ currencies via ACH, wire, and eCheck

- KPMG-approved tax and VAT compliance with automated 1099/1042-S reporting

- Supplier portal for self-service onboarding, banking updates, and payment tracking

Pricing:

- Starter: from $99/month platform fee; custom quotes for Premium and Elite plans

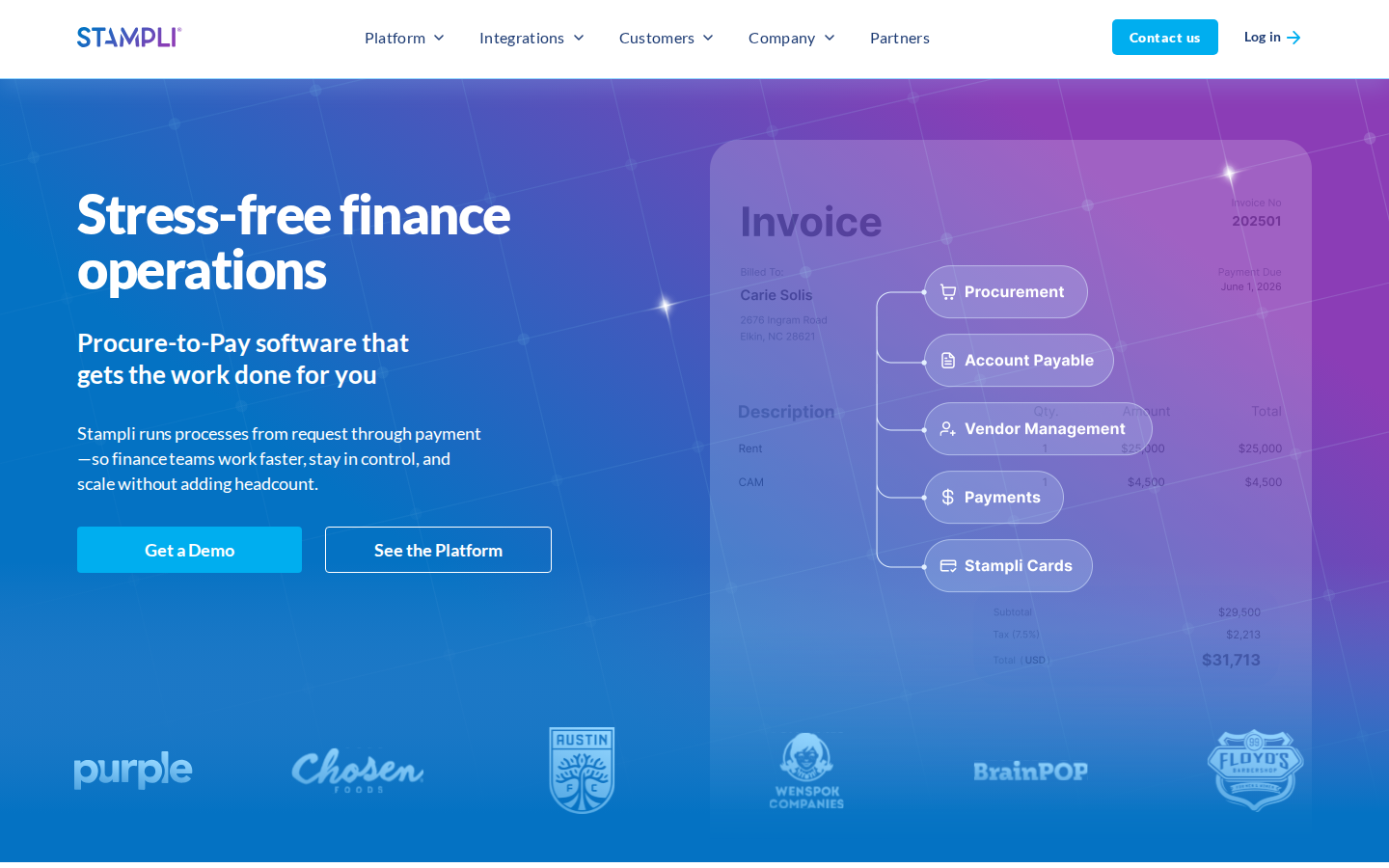

5. Stampli

Best for: Small to mid-size teams that need collaborative, communicative invoice approval workflows without disrupting their existing accounting system

Bill.com vs. Stampli: Stampli's in-invoice communication threads allow approvers to discuss and resolve questions directly on an invoice, a collaborative layer that BILL's approval workflow does not replicate.

Stampli is designed around the idea that AP friction usually comes from communication breakdowns during the approval process. Its “Billy the Bot” AI assistant learns your coding patterns and suggests GL codes, cost centers, and approvers automatically. Approvers can ask questions, add comments, and resolve issues directly inside the invoice interface rather than trading emails.

Stampli is ERP-agnostic, with integrations for more than 70 accounting and ERP systems, including QuickBooks, Xero, NetSuite, Sage Intacct, and Microsoft Dynamics. Implementation is notably fast compared to enterprise alternatives like Tipalti, and the platform can often be deployed in a matter of days.

The trade-off is that Stampli focuses primarily on AP rather than a broader financial operations platform. It does not include corporate cards, banking, lending, or meaningful AR automation. Pricing is not published and requires a demo request, which makes upfront budgeting difficult.

Stampli earns a 4.6 out of 5 on G2. Users consistently highlight the quality of the customer support team and the speed of ERP deployment as highlights, while noting that reporting customization can feel limited.

Key features:

- Billy the Bot AI for automated GL coding, routing, and duplicate detection

- In-invoice communication threads for approvers and AP teams

- 70+ native ERP integrations with fast, in-house deployment

Pricing:

- Custom pricing; contact Stampli for a quote

6. Brex

Best for: Venture-backed startups and high-growth companies that need corporate cards, spend controls, and global financial infrastructure without a personal guarantee

Bill.com vs. Brex: Brex includes corporate cards, global reimbursements, and treasury features in addition to bill pay, covering a broader scope of corporate spend than BILL's AP/AR focus.

Brex is a corporate financial platform designed for startups and scaling companies with venture backing or significant capital. Its corporate cards require no personal guarantee, which is an important feature for founders who do not want to tie their personal credit to company spend. Brex has expanded from cards into a broader platform that includes bill pay, travel management, expense reimbursement, and treasury management.

For companies already operating across borders, Brex supports multi-currency accounts, global reimbursements, and native ERP integrations with NetSuite, Workday, and Sage Intacct. The platform is particularly strong for companies using these enterprise systems, where BILL's integration depth is more limited.

Brex is not accessible to all business types. The platform targets incorporated businesses, particularly those with institutional investors or significant monthly spend, and does not typically serve sole proprietors or very early-stage businesses. Customer support response times at scale have drawn some criticism.

Brex earns a 4.6 out of 5 on G2. Users frequently praise the card rewards program and the quality of the NetSuite integration, with some noting that the platform's complexity can be overkill for smaller teams.

Key features:

- Corporate cards with no personal guarantee and high credit limits

- Global reimbursements, spend controls, and multi-currency treasury

- Native integrations with NetSuite, Workday, and Sage Intacct

Pricing:

- Starter: Free

- Premium/Enterprise: Custom pricing

7. QuickBooks Online

Best for: Small businesses that want their general ledger, AP, AR, payroll, and reporting inside a single accounting platform

Bill.com vs. QuickBooks Online: QuickBooks Online includes accounting, invoicing, and bill pay natively, eliminating the need to sync a separate AP tool with your books the way BILL requires.

QuickBooks Online is the most widely used small business accounting platform in the U.S., and it serves as the general ledger backbone for millions of businesses. Because BILL is often used as an add-on layer on top of QuickBooks, businesses that want to simplify their stack sometimes find it more efficient to lean into QuickBooks' built-in AP and invoicing features rather than pay for a separate AP tool.

QuickBooks Online's bill pay handles basic vendor payments, and its invoicing tools cover the needs of most service businesses. Advanced plans include receipt capture, mileage tracking, project profitability reporting, and inventory management. The Payroll add-on integrates directly with the general ledger.

The limitation compared to BILL is that QuickBooks Online is an accounting and record-keeping platform first. Its AP automation is functional but does not offer the same approval workflow depth, payment method flexibility, or vendor management features that dedicated AP tools like BILL or Stampli provide. Multi-entity support is also limited compared to mid-market AP platforms.

QuickBooks Online earns a 4.3 out of 5 on Trustpilot. Users value the breadth of the accounting feature set and the large ecosystem of integrations and accountant support, while common criticisms center on pricing increases and customer support response times.

Key features:

- Full general ledger with AP, AR, and bank reconciliation in one platform

- Payroll, mileage tracking, inventory, and project profitability on higher plans

- Extensive accountant network and 750+ app integrations

Pricing:

- Simple Start: $30/month

- Essentials: $55/month

- Plus: $85/month

- Advanced: $200/month

8. AvidXchange

Best for: Middle-market companies in real estate, construction, HOA management, and property-related industries

Bill.com vs. AvidXchange: AvidXchange offers industry-specific AP workflows tailored to real estate and construction that BILL's more generic platform does not provide.

AvidXchange is an AP automation and payment platform targeted at middle-market companies, with particular depth in real estate, property management, construction, and HOA management. The platform offers over 800 integrations with property management systems and construction ERP tools, including Yardi, MRI Software, and Sage 300 CRE, which are not available in BILL.

AvidXchange handles check outsourcing, virtual card payments, and ACH transfers, and its payment network includes a large base of suppliers already enrolled for electronic payment. For businesses in its target industries, the pre-built workflow templates and deep vertical integrations can dramatically reduce implementation time.

AvidXchange is less suitable outside its core verticals and is not designed for very small businesses. Pricing is custom and not published, which adds friction to the evaluation process. Some users report that the interface feels dated and that configuration for complex approval workflows requires significant setup effort.

AvidXchange earns a 4.3 out of 5 on G2. Users in property management and construction highlight the vertical-specific integrations and the supplier payment network as the platform's most compelling advantages.

Key features:

- Industry-specific AP workflows for real estate, construction, and HOA management

- Pay-by-check outsourcing, virtual card, and ACH payment services

- 800+ integrations with property management and construction ERP systems

Pricing:

- Custom; contact AvidXchange for a quote

How to find the best financial operations platform for your small business

Choosing between BILL and its alternatives comes down to a few key questions about how your business operates and what you need your financial platform to do beyond paying vendors.

- Decide whether you need banking alongside your AP/AR tools: If you want a single platform that handles both your operating account and your payables workflow, a dedicated business banking platform like Bluevine is a better fit than a standalone AP tool. Bluevine offers FDIC insurance up to $3 million through Coastal Community Bank, Member FDIC and partner banks2, up to 3.0% APY on checking balances1, and integrated bill pay and invoicing, eliminating the need to manage a bank account and an AP tool separately.

- Match pricing structure to your team size: Per-user pricing (like BILL's $45 to $89 per user per month) scales in a predictable but expensive way for teams with more than a handful of users. Flat-rate alternatives like Melio's Unlimited plan ($80/month for unlimited users and ACH transfers) or no-software-fee tools like Ramp may be more cost-effective depending on your headcount.

- Consider whether you need global payments: For businesses paying suppliers internationally, Tipalti's support for 196 countries and 120+ currencies, combined with built-in tax compliance, is hard to match. For domestic operations, simpler tools like Melio or Bluevine’s integrated bill pay will cover the workflow.

- Evaluate cash flow tools: Access to lending products matters for businesses that need working capital. Most AP/AR platforms, including BILL, do not offer loans or lines of credit. Bluevine's integrated checking account gives eligible businesses access to apply for a line of credit up to $250,000 and term loans through partners for approved customers3, alongside their operating account.

- Check support for your business structure: Some platforms are restricted to incorporated businesses. Bluevine accepts sole proprietors, LLCs, partnerships, S-corps, C-corps, and other structures, making it accessible to a wide range of business types. If you are a sole proprietor or run a newer business, confirm that any platform you evaluate accepts your structure before committing.

Better banking starts with the right foundation

The right alternative to BILL depends on whether you need pure AP/AR automation, a banking platform with payment tools built in, or something in between. For businesses looking to earn interest on operating balances, access cash deposit networks, and keep their invoicing and bill pay inside the same account, Bluevine is designed to do all of that. Eligible businesses earn up to 3.0% APY1 on checking balances, get FDIC coverage up to $3 million through Coastal Community Bank, Member FDIC and partner banks2, and can access cash deposits at over 90,000 Allpoint+ and Green Dot® locations4, with no need to manage a separate bank.

FAQs

answer

Disclaimers

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

Ratings as of March 2026.

1. Bluevine Premier customers will earn 3.0% annual percentage yield ("APY") on total Bluevine Business Checking balances. Any interest accrued and payable for an account or sub-account will be paid to your main account. Enrollment in Bluevine Premier is not required to receive increased FDIC insurance coverage. Customers automatically receive increased FDIC coverage unless they have opted out of the Bluevine Business Checking Account Agreement Sweep Program.

2. Bluevine accounts are FDIC insured up to $3,000,000 per depositor through Coastal Community Bank, Member FDIC and our program banks. $3,000,000 in FDIC insurance is offered by multiplying the standard $250,000 FDIC coverage across multiple banks.

3. Applications are subject to credit approval. Rates, credit lines, and terms may vary based on your creditworthiness and are subject to change. Eligibility for the lowest rates is available only to applicants with the strongest credit profiles. Factors include FICO score, time in business, monthly revenue, and payment history. Additional fees apply. Bluevine Flex Line of Credit is issued by Celtic Bank, a Utah-chartered Industrial Bank, Member FDIC.

4. A $4.95 per transaction fee is applicable when depositing funds at Green Dot® locations. A fee of $1.00 plus 0.5% of your total deposit amount applies when depositing funds at Allpoint+ ATMs.

5. Payment processing services are provided by Stripe, Inc., N.A. Bluevine Inc. Payment processing services are available to most businesses, subject to eligibility determined by Bluevine.

6. Draw requests are subject to review and approval. Bluevine Line of Credit customers can access approved draws instantly only with their Bluevine Business Checking account. Approved draws being deposited to an external bank account will be available in as quickly as a few hours if you choose our bank wire option ($15). Or, choose our fee-free ACH transfer option which typically gets funds deposited the next business day, although it may take up to three. Bluevine Flex Line of Credit is issued by Celtic Bank, a Utah-chartered Industrial Bank, Member FDIC.

7. Bluevine Plus is subject to a $30 monthly fee. Avoid the fee by doing the following each billing period: 1) maintain an average daily balance of at least $20,000 in your Bluevine Business Checking account and/or sub-account(s) and 2) spend at least $2,000 with your Bluevine Business Debit Mastercard® or Bluevine Business Cashback Mastercard®.

8. Bluevine Premier is subject to a $95 monthly fee. Avoid the fee by doing the following each billing period: 1) maintain an average daily balance of at least $100,000 in your Bluevine Business Checking account and/or sub-account(s) and 2) spend at least $5,000 with your Bluevine Business Debit Mastercard® or Bluevine Business Cashback Mastercard®.

Bluevine is a financial technology company, not a bank. Banking Services provided by Coastal Community Bank, Member FDIC. FDIC insurance only covers the failure of an FDIC-insured bank. FDIC insurance is available through pass-through insurance at Coastal Community Bank, Member FDIC, if certain conditions have been met. Bluevine accounts are FDIC insured up to $3,000,000 per depositor through Coastal Community Bank, Member FDIC and our program banks. The Bluevine Business Debit Mastercard® and Bluevine Business Cashback Mastercard® are issued by Coastal Community Bank, Member FDIC pursuant to a license from Mastercard International Incorporated and may be used everywhere Mastercard is accepted. Mastercard is a registered trademark and the circles design is a trademark of Mastercard International Incorporated.

Mastercard, Mastercard Easy Savings, Mastercard Airport Concierge, Priceless Surprises and the circles design are registered trademarks and Mastercard ID Theft Protection is a trademark of Mastercard International Incorporated.

Application is subject to approval. No monthly or maintenance fees. Card Replacement Fees and Wire Transfer Fees may apply.

Banking Services for payments made via ACH or wire from the Bluevine Business Checking Account are provided by Coastal Community Bank, Member FDIC. Money transmission services for International Payments are provided by a third party and are also subject to their applicable terms and conditions.

The Bluevine Line of Credit is issued by Celtic Bank and is serviced by Bluevine. Applications are subject to credit approval. Rates, credit lines, and terms may vary based on your creditworthiness and are subject to change. Additional fees apply. Other commercial credit products are offered by a variety of Bluevine’s third party partners. Bluevine is not involved in the issuance or servicing of these products. Offerings and eligibility requirements vary by partner.

Certain financing may be made or arranged pursuant to California Financing Law-License No. 6054789.

Payment processing services are provided by Stripe, Inc., N.A. Bluevine Inc. Payment processing services are available to most businesses, subject to eligibility determined by Bluevine.

Tap to Pay is only available on supported devices and may require upgrading to the latest version of the Bluevine app and your phone’s operating system. Some Android devices may not be compatible. Android is a trademark of Google LLC. Tap to Pay on iPhone requires a supported payment app. Some contactless cards may not be accepted by your payment app. Transaction limits may apply. The Contactless Symbol is a trademark owned by and used with permission of EMVCo, LLC. Tap to Pay on iPhone is not available in all markets. For Tap to Pay on iPhone countries and regions, see here.

All other product names, logos, brands, trademarks, and registered trademarks are property of their respective owners. All company, product, and service names used in this website are for identification purposes only. Use of these names, trademarks, and brands does not imply endorsement.

® 2026 Bluevine Inc. All Rights Reserved. “Bluevine” and the Bluevine logo are registered trademarks of Bluevine Inc.