Working capital management is how a business manages its short-term cash, such as money received from customers and money paid to cover expenses. The goal of your working capital management is to keep enough cash on hand to run your business smoothly.

Cash flow issues (late customer payments, unused inventory, clunky payables) make it hard to see how much cash you have available. Working capital management helps businesses track and control cash flow, so you can cover expenses and avoid unnecessary financial strain. When working capital is managed well, businesses can pay bills on time and make informed decisions about growth. It makes cash flow consistent and predictable, which reduces financial risk and supports long-term stability.

This guide explains what working capital management is, how to measure it, and practical ways to manage it effectively.

What you need to know

Effective working capital management keeps cash flowing, reduces financial risk, and supports business growth.

Key strategies include optimizing receivables and payables, managing inventory, tracking KPIs, and leveraging automation or technology for efficiency.

Flexible financing, like a Bluevine Line of Credit, can give your business quick access to much-needed capital.

Working capital management is the practice of monitoring, optimizing, and balancing your company’s immediate assets and liabilities to make sure you have cash when you need it. It involves managing inventory, accounts receivable (AR), and accounts payable (AP) at a ratio that ensures liquidity for short-term and long-term business goals.

Effective working capital management minimizes financial risk while keeping enough cash on hand for daily operations. Without this balance, your business may have to cut payroll, marketing, customer support, or other essentials, which limits your ability to grow and adapt.

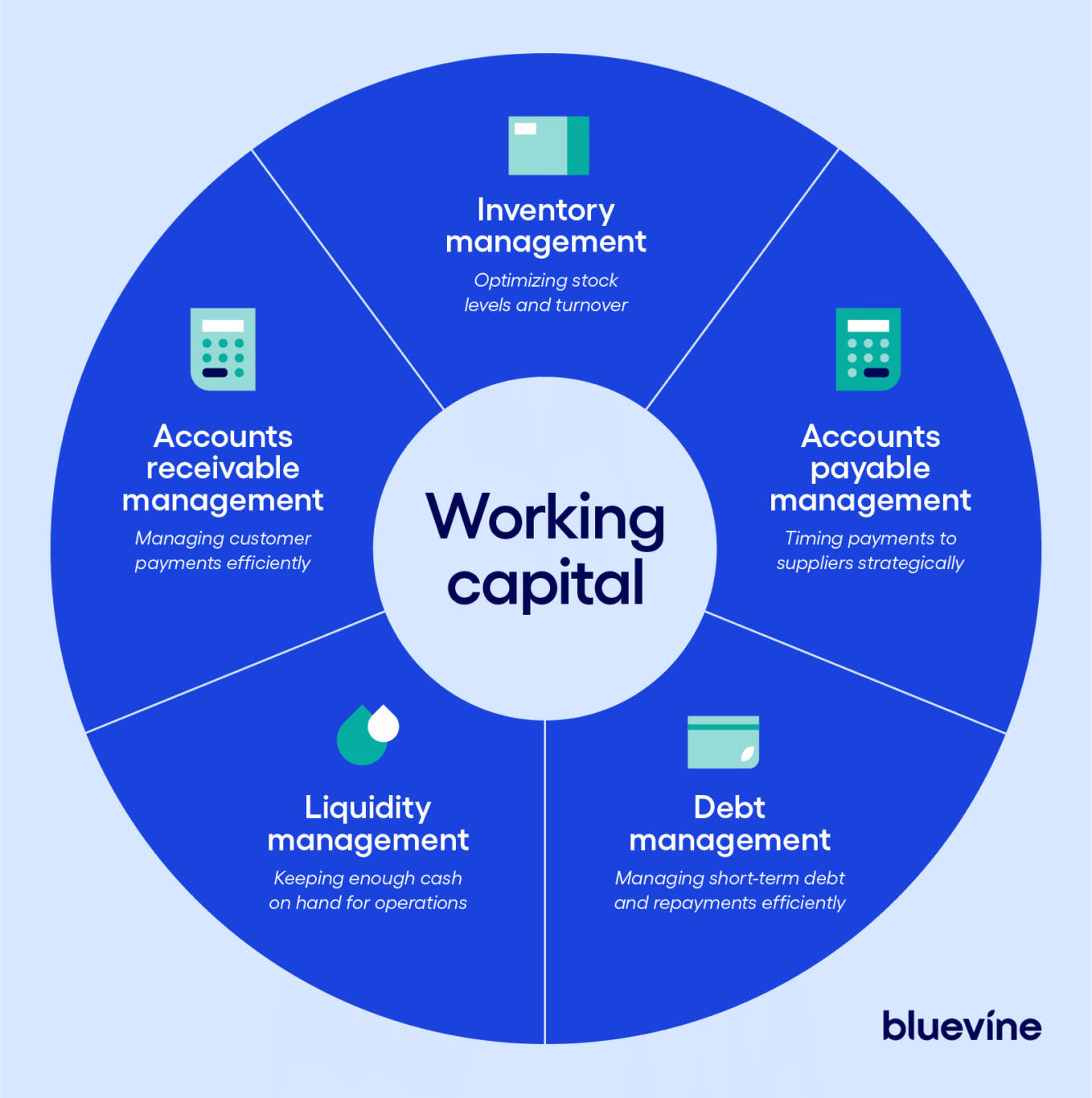

These five components typically impact your working capital management the most:

Liquidity management: Knowing how much cash you have on hand and making sure it’s available when you need it. Poor visibility here can lead to missed payments or last-minute financing.

Accounts receivable management: How quickly customers pay you. Late or inconsistent payments tie up cash, and can create gaps between revenue and having funds available.

Inventory management: Making sure inventory levels match demand. Overstocking ties up cash in unsold goods, while understocking can lose sales and disrupt operations.

Accounts payable management: Managing when you pay vendors and suppliers. Paying too early can drain cash, while paying too late can strain relationships and ripple across your own finances.

Debt management: Repaying your business loans and credit on-time. Smart debt management avoids insolvency and builds business credit, which can qualify you for better terms with lenders and vendors.

The formula for working capital

Working capital = Current assets – Current liabilities.

–

Current assets include cash, money owed by customers (accounts receivable), and inventory that can be sold quickly. Current liabilities include bills, short-term loans, accounts payable to vendors, credit card balances, payroll, rent, or lease payments.

The result of the working capital formula tells you whether your business has enough short-term resources to cover obligations. For example:

Positive working capital means you can pay bills, restock inventory, and cover unexpected expenses without borrowing.

Negative working capital signals potential cash flow problems—you might need to delay payments, secure short-term financing, or adjust operations to avoid crunches.

The importance of working capital management

Effective working capital management helps businesses maximize their short-term assets and liabilities. Here’s how it helps in practice:

Improves liquidity: Working capital management makes clear how quickly cash is moving in and out of your business. Shortening the time between paying expenses and collecting revenue helps you keep more usable cash on hand to cover payroll, rent, and surprise costs without relying on emergency financing.

Reduces financial and operational risk: When your receivables, payables, inventory, and short-term debt tracking is out of sync, you may accidentally overbuy inventory or take on debt your business can’t repay. Managing receivables, payables, inventory, and short-term debt together helps you avoid these mistakes.

Strengthens cash flow control: Working capital management shows where cash is getting stuck, whether in unpaid invoices, excess inventory, or early vendor payments. By doing so, you can fix bottlenecks before they create cash shortages.

Supports sustainable growth: Growth requires cash up-front, before your business generates revenue from your investment. Working capital management ensures you can fund growth plans without growing faster than your cashflow allows.

Types of working capital

Knowing the different types of working capital will help you see how your business uses cash and plan for growth or unexpected expenses. Here are the main types:

Gross working capital: The total value of a company’s current assets, including cash, accounts receivable, and inventory. It shows how much short-term value the business controls, not including liabilities.

Permanent working capital: The minimum level of working capital a business needs to operate consistently. This amount stays relatively stable and supports ongoing expenses like payroll, utilities, and baseline inventory.

Temporary working capital: Additional working capital needed to handle short-term increases in demand, such as seasonal spikes or promotions. It fluctuates based on business cycles.

Regular working capital: The portion of working capital used for routine, regular expenses. It ensures your business can run smoothly under normal conditions.

Reserve margin working capital: Extra cash set aside for unexpected events. It’s a buffer to reduce risk during financial disruptions.

Important working capital metrics

These key working capital ratios indicate whether your business has enough liquidity, how efficiently it’s using assets, and how quickly cash is moving through operations. Monitoring these ratios will help you spot potential cash flow problems before they become urgent.

<1 = relies on inventory or financing ≥1 = can meet obligations with liquid assets

Working capital turnover

Industry-dependent

Low = capital tied up Very high = potential under-investment

Cash conversion cycle (CCC)

Shorter than industry peers (ideally under 60 days)

<30 days = excellent 30–60 = healthy 60–90 = slow 90+ = red flag

1. Current ratio

The current ratio is calculated as Current Assets ÷ Current Liabilities. It shows whether a business has enough short-term assets to pay for short-term obligations. A ratio above 1.0 indicates that the company can pay its bills without issue, while a ratio below 1.0 signals liquidity problems.

Bluevine Tip

Current ratio is a quick health check for day-to-day operations. If the ratio is consistently low, you should review cash flow, reduce short-term liabilities, or find ways to free up assets to avoid cash crunches.

2. Quick ratio

The quick ratio is calculated as (Current assets – Inventory) ÷ Current liabilities. It focuses on the most liquid assets, excluding inventory, to assess the company’s ability to pay short-term obligations quickly.

A ratio above 1.0 indicates good short-term financial health, while a ratio below 1.0 suggests the business may struggle to meet immediate payments.

3. Working capital turnover ratio

The working capital turnover ratio is calculated as Net sales ÷ Average working capital. It measures how efficiently a company uses its working capital to generate revenue.

A higher ratio indicates that assets and liabilities are being effectively converted into sales, while a lower ratio signals that resources may be underused.

4. Cash conversion cycle

The cash conversion cycle (CCC) measures how long it takes for cash invested in operations to return as revenue. It’s calculated as: Days Inventory Outstanding (DIO) + Days Sales Outstanding (DSO) – Days Payable Outstanding (DPO).

DIO tracks how long inventory sits before being sold.

DSO measures how long it takes customers to pay.

DPO shows how long the business takes to pay its own bills.

Did you know?

With a Bluevine Business Checking account, your business can earn high APY on working capital while keeping funds liquid and accessible for day-to-day operations.

Tips to manage working capital effectively

Managing working capital helps your business avoid surprises and make informed decisions. These tips show practical ways to improve cash flow and use short-term assets more effectively.

Use financial forecasting and automation tools

Cash flow forecasting and real-time dashboards show where your money is and where it’s going. With this visibility, you can schedule payments and purchases, allocate cash, and prevent idle money or shortfalls. Automation tools also save time and reduce mistakes in accounts receivable and accounts payable management.

Optimize inventory management

Keep the right amount of inventory on hand. Overstocking ties up cash and increases storage costs, while stockouts can disrupt sales. Using stock analysis, demand forecasting, and automated tracking ensures you have what you need without locking up unnecessary capital.

Reduce overhead and eliminate inefficiencies

Streamline workflows, automate repetitive tasks, and cut unnecessary costs. Lowering overhead frees up cash for daily operations and growth opportunities, while simplifying processes reduces mistakes and delays.

Improve vendor management practices

Work with vendors to get better terms and save money. Renegotiate contracts, consolidate suppliers, or secure early-payment or volume discounts. Strong vendor relationships and better contract management free up capital and reduce surprises.

Track working capital KPIs

Monitor key metrics, like days sales outstanding (DSO), days payable outstanding (DPO), inventory turnover, and the cash conversion cycle. Tracking KPIs lets you spot issues early, remove bottlenecks, and improve procedures so your cash works efficiently.

Bluevine helps small businesses access the working capital they need through lines of credit, as well as term loans from our partners—all with one simple financing application.

Strengthen your working capital with a business line of credit

Strong working capital management ensures your business always has cash available to cover expenses and unexpected costs. Even with great cash flow management practices, gaps can happen—that’s where a flexible financing option makes a difference.

A Bluevine Line of Credit gives your business fast, flexible access to funds whenever you need them. Use it to pay bills, manage payroll, restock inventory, or invest in new opportunities without waiting for revenue to arrive.BVSUP-00127

Apply for multiple financing options with no impact to your credit score.BVSUP-00128

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

Get answers in a snap, right from your dashboard during business hours.

Disclaimer

This content is for educational purposes only and should not be construed as professional advice of any type, such as financial, legal, tax, or accounting advice. This content does not necessarily state or reflect the views of Bluevine or its partners. Please consult with an expert if you need specific advice for your business. For information about Bluevine products and services, please visit the Bluevine FAQ page.

Subscribe to our monthly email newsletter.

Be the first to hear about Bluevine’s latest tips, insights, and product offerings.

Bluevine is a financial technology company, not a bank. Banking services provided by Coastal Community Bank, Member FDIC. Not all features available in all countries. Limitations apply. See international features for details.