A business line of credit is a revolving financing tool that gives your business access to a set credit limit, so you can draw funds when you need them and repay only what you use. It is commonly used to cover cash flow gaps, seasonal needs, and emergency expenses without taking on a full lump-sum loan.

What you need to know

- A business line of credit is a revolving pool of funds you can draw from, repay, and use again.

- They are a strong fit for covering cash flow gaps, seasonal fluctuations, and emergency operating expenses.

- Secured lines require collateral. Unsecured lines usually cost more and can be more difficult to qualify for.

- Applying for a Bluevine Line of Credit requires a 625+ FICO score, $10,000 in monthly revenue, and 12+ months in business.

- A term loan is a better fit for one-time, planned expenses, while a line of credit is better for flexible working capital.

How does a business line of credit work?

A business line of credit usually has a draw period and a repayment period. During the draw period, which commonly lasts 6–24 months, you can take money from your available credit up to your limit. As you repay what you borrowed, that credit replenishes, which is why a line of credit is revolving rather than installment-based. When the draw period ends, you typically can’t take new draws and must pay back the outstanding balance. That structure makes a working capital line of credit useful when your cash needs come and go over time.

Most lines of credit charge interest only on the amount you draw, not the full limit you were approved for. Depending on the lender, repayment may be interest-only during the draw period or a mix of principal and interest on a fixed weekly or monthly schedule.

A revolving line of credit lets you borrow again as you repay, while a non-revolving line does not restore the credit you used. In practice, most business owners compare revolving credit lines against installment products like term loans—think of a line of credit as flexible working capital that can be reused, not a one-and-done loan.

Types of business lines of credit

The two core types are secured and unsecured. A secured business line of credit requires collateral, such as inventory, equipment, receivables, property, or even a business bank account. Because collateral lowers lender risk, secured lines often come with higher credit limits and lower rates. An unsecured business line of credit does not require collateral, which usually makes it more expensive and sometimes harder to qualify for.

| How it works | The tradeoff | Good for | |

|---|---|---|---|

| Secured business line of credit | You post collateral in case you can’t repay the credit line. | Lower rates, higher limits, more lenient approval standards. | When you have business assets to pledge and want more favorable rates. |

| Unsecured business line of credit | You don’t post collateral. | Higher rates, lower limits, tighter approval standards. | When you want to avoid pledging assets, but can meet stronger credit and revenue requirements. |

Business line of credit requirements

Requirements vary by lender, but most approvals come down to four things: business credit history, time in business, revenue, and industry eligibility. Typically to qualify for a business line of credit requires a 625+ personal FICO score, 1–2 years in business, $10,000 in monthly revenue, incorporation as a corporation or LLC, no bankruptcies, good standing with the Secretary of State, and operation in an eligible U.S. state. It also requires an active bank connection or recent bank statements.

Traditional bank requirements are usually stricter, requiring strong personal credit, two years of business history, and healthy revenue before approving a line of credit. Alternative lenders can be more flexible and may approve businesses with stronger revenue but lower credit scores.

Consider your qualifications along these lines:

- Credit score: Better personal and business credit improves your odds and can improve pricing.

- Time in business: More history usually means lower risk to the lender. Many lenders want at least six months to two years; traditional banks often want around two years.

- Revenue: Lenders want evidence that your business can support repayment.

- Industry fit: Some industries are simply excluded. Common exclusions include gambling, pornography and paraphernalia, political campaigns, firearms and paraphernalia, illegal substances, controlled substances and paraphernalia, financial institutions and lenders, donation-based nonprofits, and auto dealerships.

How to get a business line of credit

To apply for a business line of credit, start by gathering the basics: business bank statements, proof of revenue, identification, and, depending on the lender, formation documents, tax returns, business licenses, or permits. Next, choose the lender that matches your business profile. Online lenders usually move faster and ask for less paperwork, while banks often take longer and review more deeply.

Apply online, upload your documents, and be ready for a short review of your revenue and bank activity. Once approved, the lender will set your credit limit and repayment schedule, and you can draw funds as needed from your available balance.

For additional insight, see our guide for how to get a business line of credit.

Apply in five minutes with no impact to your credit score.BVSUP-00008

How much does a business line of credit cost?

The cost of a business line of credit usually comes from interest on the amount you draw, plus any lender fees such as draw fees, maintenance fees, annual fees, late fees, or origination fees. Some lenders also charge prepayment fees, while others do not.

For example, if you draw $30,000 at 10% annual percentage rate (APR) and don’t repay that sum for a full year, you would owe about $3,000 in simple interest, plus any lender fees. If you repay faster, your interest cost drops because you are only paying for the time the funds are outstanding—the main reason a line of credit can be more efficient than borrowing a lump sum you don’t fully need.

Pros and cons of a business line of credit

Pros

- You can borrow only what you need, when you need it.

- The credit replenishes as you repay, so the same line can keep supporting future expenses.

- It works well for cash flow gaps, seasonal inventory, payroll timing, and emergency spending.

- It can help build business credit when you repay on time.

Cons

- Many lenders require strong credit, solid revenue, and time in business.

- Some lines require collateral, and unsecured lines often cost more.

- Fees can stack up depending on the lender.

- Approval can be harder for newer businesses or higher-risk industries.

When a line of credit is the right tool

- You need to cover short-term cash flow gaps between paying vendors and getting paid.

- Your sales are seasonal and inventory or payroll needs change month to month.

- You want quick access to working capital without taking a full lump sum.

- You want a financing tool that can keep revolving as you repay it.

When something else may work better

- A term loan is usually a better fit for a large one-time purchase or project with a clear budget.

- Equipment financing may make more sense if the equipment itself is the asset being funded.

- An SBA loan may be better for longer-term capital needs when you want a more structured repayment path and can tolerate a slower process.

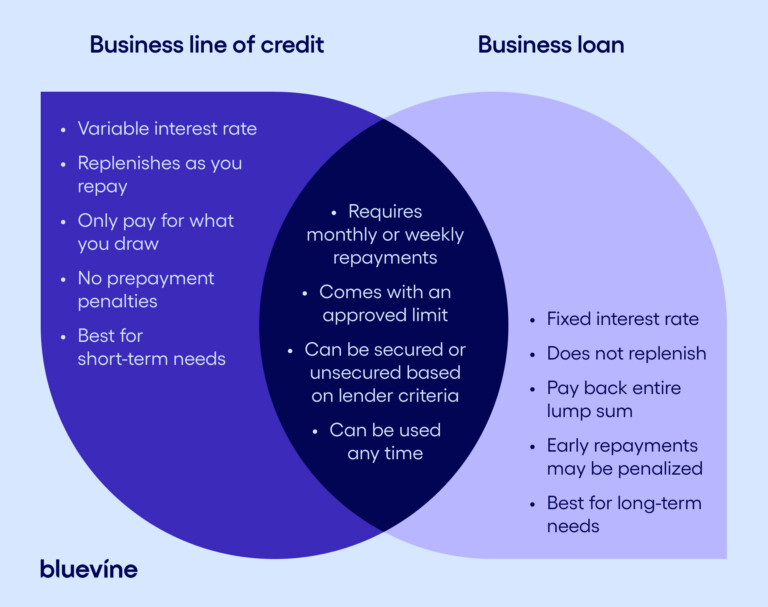

Business line of credit vs term loan

A business line of credit and a term loan solve different problems. If you need recurring access to capital, the line of credit is usually the more useful tool. If you need one lump sum for one project, the term loan is usually the cleaner fit.

| Feature | Business line of credit | Business term loan |

|---|---|---|

| Structure | Revolving credit with an approved limit you can draw against repeatedly. | Lump sum borrowed once and repaid on a set schedule. |

| Repayment | You repay what you draw, and available credit replenishes as you pay it back. | You repay principal plus interest in fixed installments. |

| Best use case | Ongoing working capital, seasonal swings, and recurring short-term needs. | One-time projects, equipment, renovations, and other planned investments. |

| Access to funds | Draw as needed, subject to lender approval. | Receive the full amount up front. |

| Interest calculation | Usually applies only to the amount drawn. | Applies to the full loan balance from the start. |

| Flexibility | High | Lower |

A business line of credit is a good fit when your cash needs move around. A term loan is a good fit when the expense is large, specific, and tied to one project. The right choice depends less on the headline amount and more on how you plan to use the money.

Business line of credit FAQs

A business line of credit is a well of funds your company can pull from and use if and when you need to. A line of credit is a flexible funding method, which opens up growth opportunities that might otherwise be unavailable. For example, a line of credit can provide financial stability if you encounter unexpected expenses or seasonal fluctuations in revenue.

If you’re looking to boost growth, you can purchase more inventory or operations equipment, or fund a new marketing campaign. If you’re expanding, a line of credit can help you open a new office or location, or it can support a new product launch.

Any business line of credit will require that your business be in good standing with no bankruptcies for the past three years. Most will also require that you have a 625+ FICO score and are in business for at least 24 months and are generating $40,000 in monthly revenue.

When you submit your application, the line of credit provider will ask you for official documents with your and your business’s basic information, and a bank connection or bank statements for the past 3 months.

No—a business loan is a lump sum of money, whereas a line of credit is a long-term pool of money you can draw from upon request. Both business loans and lines of credit have to be paid back with interest. Lines of credit are typically ‘revolving,’ which means your available pool of funds replenishes as you repay what you borrowed. When you repay a business loan, you’ll have to apply for another if you need more funds.

Generally, business loans serve one purpose and lines of credit another. Loans are good for financing specific projects that require an upfront investment. Lines of credit are better suited for long-term support, such as during sales slumps or emergencies.