For some entrepreneurs, seasonal and economic change can often lead to ups and downs in business. Sales could be robust one month, but sluggish the next.

With seasonality, let’s take summer as a prime example. If you run a store specializing in outdoor gear like grills, deck furniture, and more, money could soon be rushing in, but for holiday toy makers it’s almost certainly a lean time.

On the topic of economic downturns, customer sales or foot traffic could drastically impact revenues—whereas sudden upticks could spark a rise in demand.

Whatever the case may be for your small business, you’ll want to be prepared with the right cash flow and inventory levels, so you can survive and thrive for years to come. With that, here are six ways to manage seasonal and economic change.

1. Build a business emergency fund

The idea of an emergency fund is well-known in the personal finance space. It’s important to have a reserve of cash you can tap into in case you lose your job, your vehicle breaks down, there’s a medical emergency, or some other disaster strikes. Business owners could take the same approach and build a fund that can help keep a financial emergency, especially one that occurs during a slow season or recession, from causing serious harm to your whole business.

With a personal emergency fund, the rule of thumb is often to have three to six months’ worth of expenses saved up. You could base how much you want to save on the length of your slow seasons and your average monthly expenses.

Small business owners who draw their income from the business may need to do double duty as they build up both personal and business emergency funds.

2. Secure a line of credit

Waiting until the last minute to look for a loan or a business line of credit can be an expensive mistake; when you’re in dire need, financing can be harder to qualify for, may cost more, or might take too long to actually get. To avoid this, secure a line of credit as soon as you can, even if you don’t plan on tapping it right away.

You can then borrow money against your line of credit during lean months, in the ramp up to your busy season, or if demand suddenly spikes and you need to quickly increase supply. With line of credit providers like Bluevine, , there aren’t any annual or monthly maintenance fees, and you’ll only pay if and when you draw on the credit line.

3. Collect data to help forecast needs and prepare for lulls

Managing cash flow is important for every business, although longer lulls are expected for seasonal businesses as well as most businesses during economic downturns. . If you don’t already have one, set up an accounting system and start closely tracking your income and expenses to know where (and when) your money moves.

The data can help you forecast your cash flow, giving you some basis for how much you need to save as well as where you might be able to cut spending. Be sure to also account for significant upcoming expenses, such as large inventory orders or necessary equipment upgrades and repairs, so you can save accordingly.

4. Ask for terms from vendors

If you’ve built solid relationships with your vendors and have a good business credit score, you may be able to ask for longer terms on your invoices.

Longer terms can be particularly helpful as you manage seasonal and economic change. If you can get 60- or 90-day terms, you could have months of productivity and you won’t have to pay every bill or expense until money is flowing in.

5. Take advantage of the ebb

Business owners certainly reap the rewards of steady and/or growing income, but there’s still opportunity to be had when things are in or near the red:

- Invest in yourself. Think back to the busiest months and identify a few areas of growth that could help make you more effective next year. There are all sorts of courses and certification programs available online. For example, a management course might teach you how to improve morale and employee productivity, or you could learn how to build and improve email newsletter campaigns.

- Look for new revenue sources. Your core offering may be tied to a specific season or when the economy is on an upswing, but you could look for other ways to make money when you’d normally experience a lull. Perhaps you sublease your store or office space, find a way to expand to a different area of the world whose seasons don’t match your own, or look into recession-proof products or services.

- Find ways to save money. You could look for ways to offset your lower income by decreasing your expenses as well. For example, you could use this time to look for inefficiencies that cost you money year-round by reviewing your subscription services, comparing vendors, and identifying ways to save on supplies.

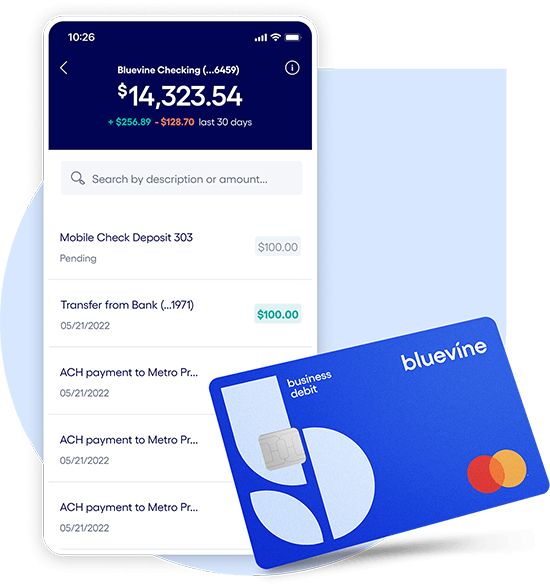

6. Use a flexible business checking account for small business

As we’ve mentioned, healthy cash flows can help your business prepare for and manage through down periods in business. At the same time, those down periods can tighten cash flow. All this to say, having flexibility in your banking is vital. That way, you won’t have to worry about meeting certain balance requirements or covering monthly or hidden fees. Instead, you can save on fees and earn interest on your balance whether you’re in a slow or busy period.

At Bluevine, we designed our Bluevine Business Checking account specifically for small businesses. There are no monthly or hidden fees, balance requirements, or transaction limits—and eligible customers earn 2.0% interest on balances up to $100,000BVSUP-00005.

Small business checking, built for your needs

Unlimited transactions, live support, high interest rates, and no monthly fees. Open a Bluevine business checking account online today.

Learn more