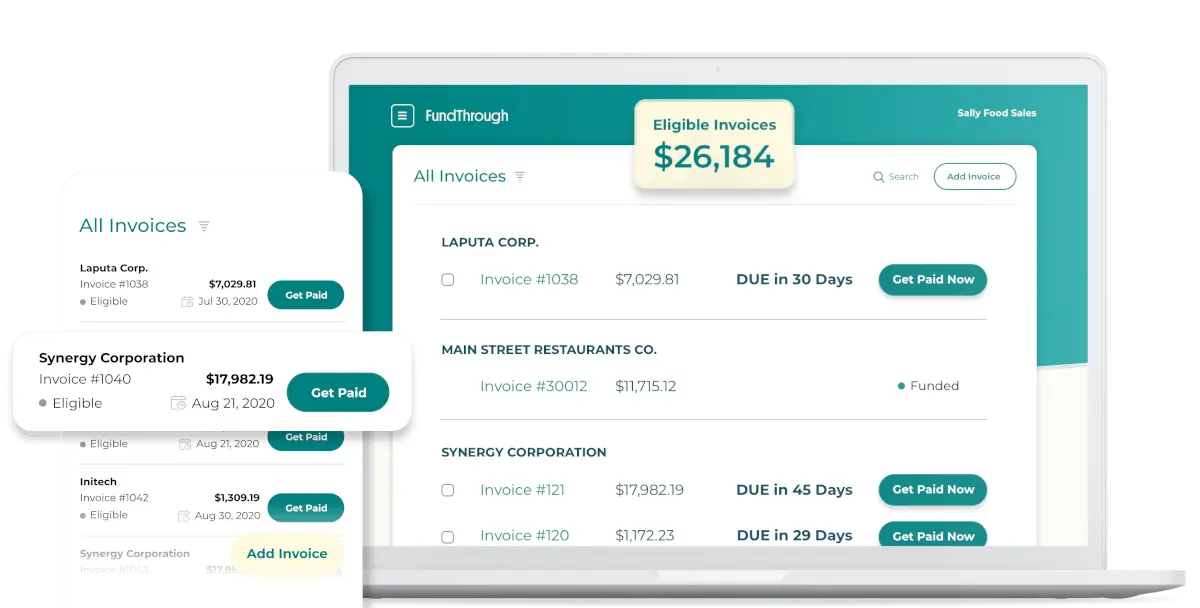

Turn unpaid invoices into working capital

Don’t wait on net terms. Get a cash advance on your

outstanding invoices with invoice factoring via FundThrough.BVSUP-00045

FundThrough helps you access

more capital with full flexibility.

Get a factoring line that grows with your business.

As your sales grow, so can your invoice factoring limit.

Free up your cash.

Unlike a traditional loan, there are no recurring payments when your customer pays by the invoice due date.

Fund only what you want.

You decide which invoices to submit, without long-term contracts.

Transparent fees.

Know exactly what you’re paying with

straightforward fees.

How Invoice Factoring Works

Apply online

Create an account with FundThrough for free and provide some basic information about your business.

Submit an invoice

Get a funding offer based on your business and customer size. Then you can select the invoices you’d like to get funded.

Get your advance

Receive payment for the full invoice (minus a fee) to your linked bank account upon approval.

What you need to get started

Have the following information handy when you’re ready to apply for invoice factoring.

- Business formation documents, like LLC certificates or

Articles of Incorporation - Government-issued photo ID, i.e., driver’s license or passport

- Voided check from your business checking account

- Recent business tax documents

Ready to apply?

Apply with FundThrough

Bluevine has partnered

with FundThrough for

invoice factoring

Free up your cash flow and apply for invoice funding on FundThrough’s website.